A year of structural change and rising enforcement

Welcome to our annual Competition and Consumer Insights report. Each year, we outline the key developments in Australian competition law and what they might mean for you in the next 12 months.

2025 was another remarkable year, with competition law and policy at the heart of conversations across Australia’s C-suites, boardrooms and BBQs. Merger reform remained a central focus, as advisers and business wrestled with the most significant and complex overhaul of merger clearance laws in Australian history.

The year also saw major developments:

Judgment was delivered in the truly Epic private section 46 litigation against Apple and Google and related class actions.

Competition law returned to the High Court for the first time in years – and not just once.

The Australian Competition and Consumer Commission (ACCC) achieved a string of high-profile and high-value penalties and proceedings against major brands under consumer law.

The Commonwealth Government continued to expand the ACCC’s powers in response to cost of living and hip-pocket concerns, with proposals to directly regulate pricing in the grocery aisle, amongst other contentious reforms.

Australia’s new merger regime is live

In 2024–2025, Australia undertook the most significant rewrite of its merger laws in 50 years.

The regime had a ‘soft launch’, with voluntary use from 1 July 2025. Since 1 January 2026, the new framework has been mandatory for all deals that satisfy the notification thresholds.

These changes have significant implications for transactions:

Revenue and transaction value thresholds are relatively low, including for global deals with even a limited business in Australia as well as a range of transactions beyond traditional M&A.

The risks of non-compliance are severe. Transactions that meet the relevant thresholds but are not properly notified are automatically treated as void, although this may be refined by legislative changes slated for later in 2026.

Substantial filing fees apply. Phase 1 filings involve a fee of $56,800; a further $475,000 to $1,595,000 is payable for a Phase 2 review, depending on transaction value; and $401,000 is payable for an optional assessment of net public benefits. Waivers are available for ‘no risk’ transactions for a fee of $8,300. Further hefty fees can apply for decisions that are referred to the Australian Competition Tribunal, with a filing fee fixed at 0.12% of transaction value, capped at $2,950,000.

Most merger parties must now factor ACCC mandatory clearance timeframes into deal planning.

The process is public, with a public register of all notified transactions and waivers.

There are significant changes in review rights, with a shift from a judicial enforcement model to the ACCC as administrative decision-maker, subject to limited merits review in the Australian Competition Tribunal.

Early indications suggest the ACCC has received more applications than anticipated. At the time of writing, it has received approximately 50 applications (29 filings and 21 waiver applications), all of which will involve the provision of some level of reasoned decisions. This already exceeds the number of published decisions under the informal clearance regime, only six weeks into operation.

It will certainly be a busy year. Given that the ACCC has a stated goal of deciding 80% of applications within 20 business days, this has driven a need for increased resourcing. The agency has already increased the headcount of its specialist mergers team from 65 to 115, with budget to further expand that to 145 in total.

As well as expanding in number, the ACCC is also deepening its pool of economic expertise and restructuring the way that merger teams operate.

For merger parties and advisors, the work and cost required to clear many transactions will also increase, including Australian aspects of global deals. The process will involve a new and different model of engagement with the ACCC, including greater upfront demands for data and evidence. The shift from an ‘enforcement’ model to an ‘administrative decision making’ model is already seeing some changes in the approach which the ACCC adopts to the process.

Several aspects of the new regime were still being refined even in the last weeks of 2025, and further changes are expected in 2026 ahead of a scheduled review of the notification thresholds after 12 months, and a more comprehensive statutory review after three years.

Increasing public merger reviews under the old framework but a decline in Phase 2s

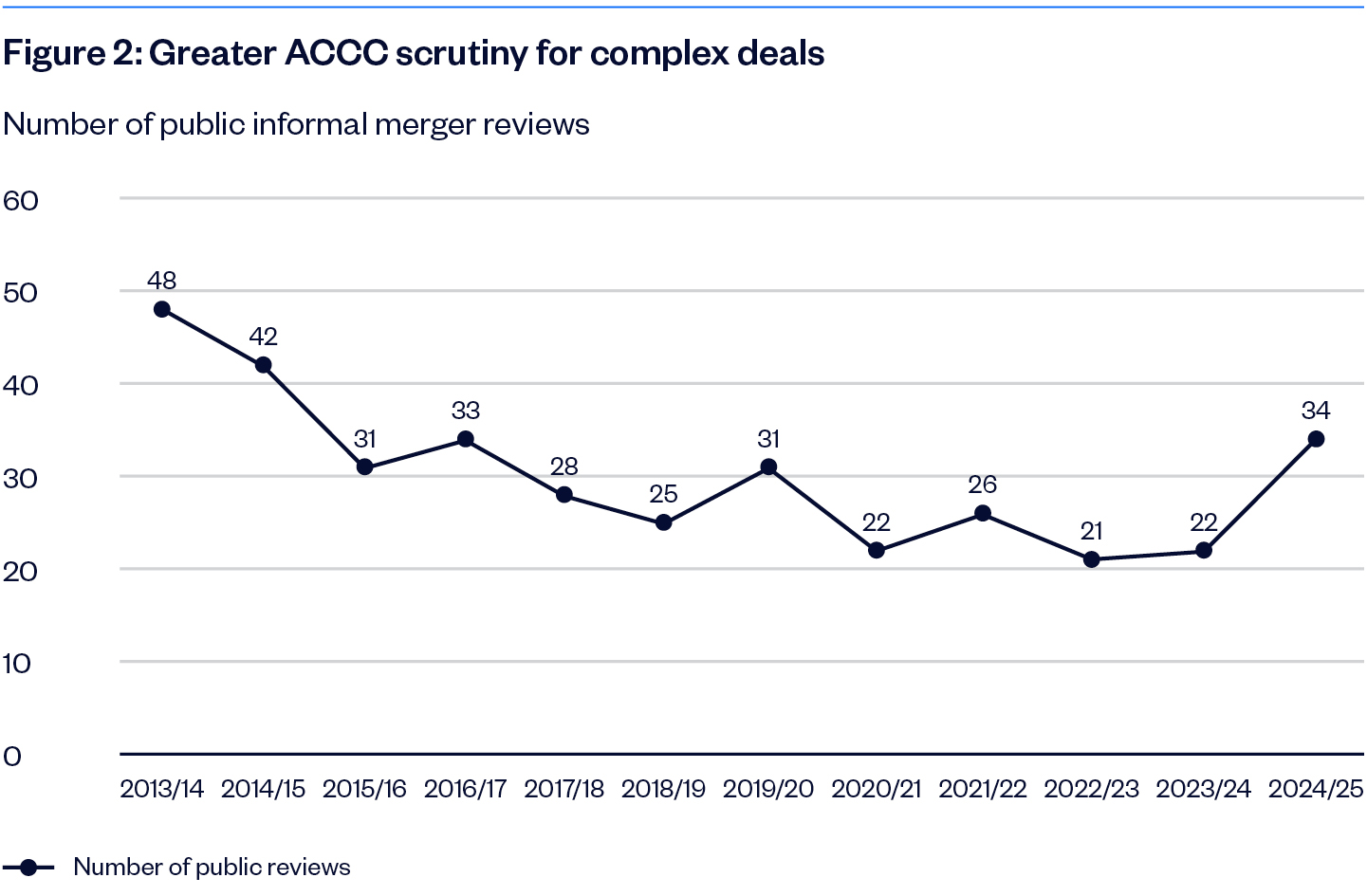

Even before the new merger regime commenced, complex transactions were subject to more scrutiny from the ACCC.

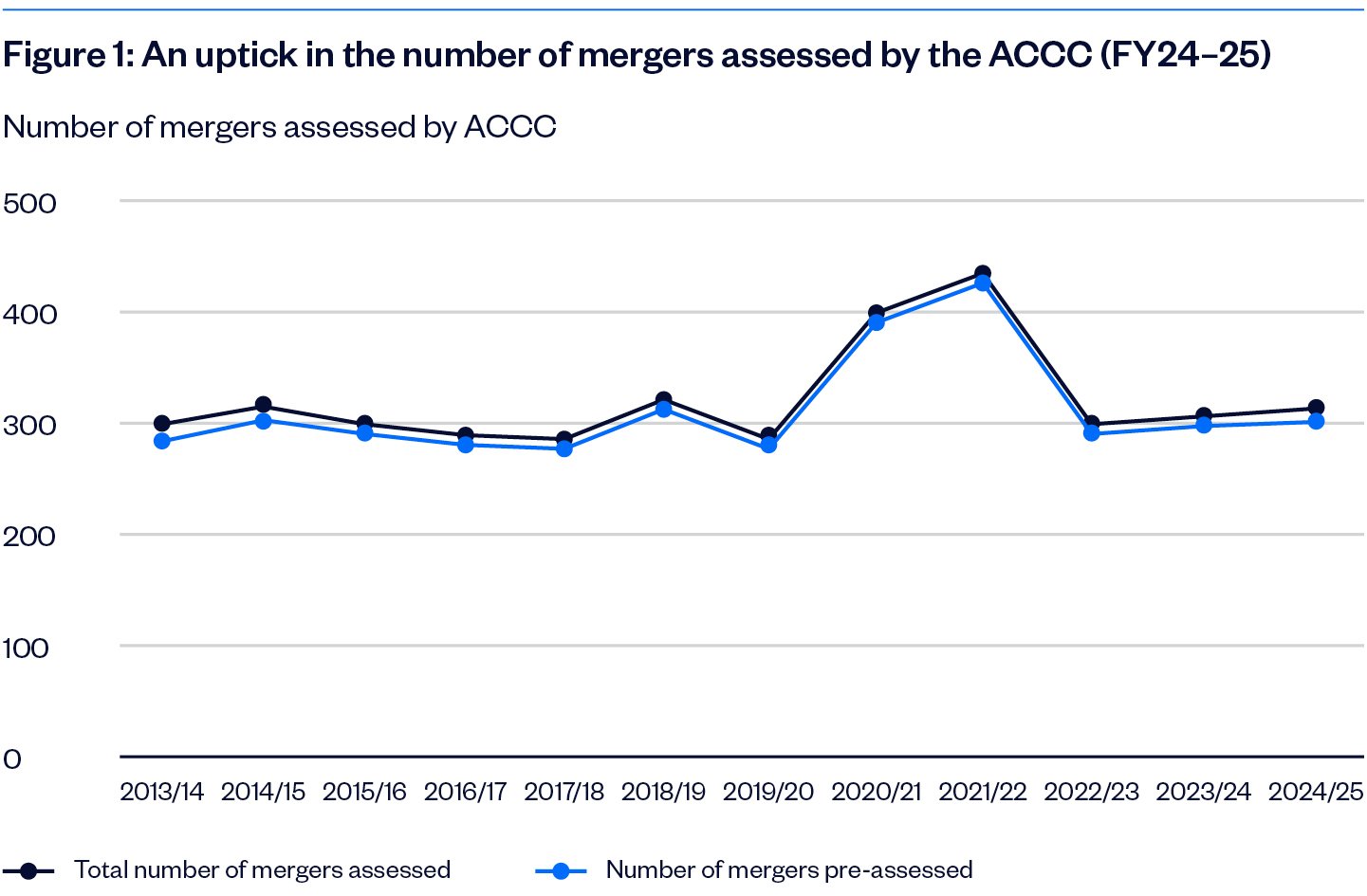

In 2024–25, the ACCC conducted 34 Phase 1 public reviews – more than in any year in the last decade. There was also a slight uptick in the overall number of mergers assessed by the ACCC (323 compared with 307 in the previous year to 30 June). 89% of those were processed through the ACCC’s fast track ‘pre-assessment’ process, which has now ended with the introduction of the new formal merger clearance regime.

However, this doesn’t tell the whole story. The last six months of 2025, which is not yet reflected in the data, saw a significant increase in parties seeking informal clearance letters that provided transitional protection from having to file under the new regime. We understand the ACCC received around 500 requests for section 189 letters before the old framework concluded.

We would expect the s189 letters are a reasonable proxy for the kind of deals that parties are likely to seek to have waivers granted. If this is the case, then the early signs are that the ACCC and Treasury have significantly under-forecast the impact of the wide scope of the regime on the number of deals that now need to be approved.

Figure 1: An uptick in the number of mergers assessed by the ACCC (FY24–25)

The trend of complex ACCC theories of harm continued

While most publicly assessed mergers involved unilateral or coordinated effects and increasingly vertical foreclosure issues, recent assessments have raised concerns about:

access to data

nascent or potential competition

ecosystems and multi-sided markets.

The ACCC is also developing a wider range of theories of harm through market inquiries and antitrust investigations. These may play a greater role in its approach to merger assessment into the future.

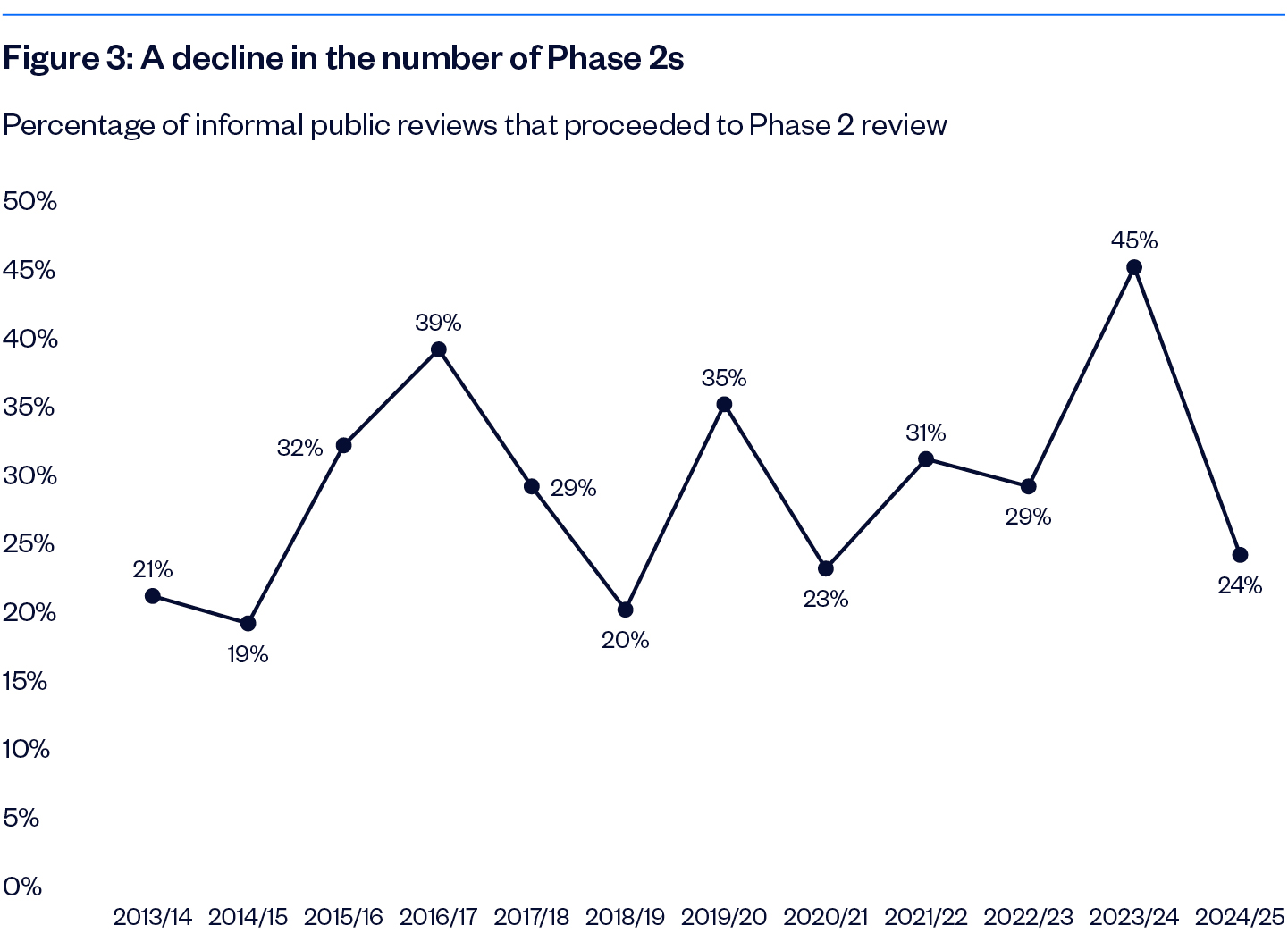

While the number of public merger reviews increased significantly in 2024-2025, the number of deals that progressed to a Phase 2 review declined slightly – there were eight Phase 2s commenced during this period, compared with 10 in the previous year. In relative terms, this means that the proportion of deals that proceeded to Phase 2 following a public review fell dramatically from 45% in 2023-2024 to 24% in 2024-2025, suggesting that increased scrutiny did not necessarily mean an extended process or a negative outcome.

Figure 2: Greater ACCC scrutiny for complex deals

Figure 3: A decline in the number of Phase 2s

Of the eleven Phase 2s completed in 2024-2025:

while none were opposed outright, two were withdrawn (Orikan / Duncan Technologies and Olam / Namoi)

five were cleared with remedies (Qube / MIRRAT, Blackstone Group / I’rom Group, Sigma / Chemist Warehouse, Stockland and Supalai / 12 MPCs from Lendlease, and LDC / Namoi)

four were cleared outright (Cleanaway / Citywide, Aurizon / Flinders, Icon Group / St Vincent’s Chermside, and Icon Group / St Andrew’s).

This paints a more positive picture in terms of overall outcomes compared with the previous year, when the ACCC was arguably responsible for ‘blocking’ eight deals.

Still, merger parties in a Phase 2 process had to work hard. So-called ‘red light’ Statements of Issues, where the ACCC indicates that it has serious competition concerns regarding a transaction, were present in 73% of Phase 2s completed in 2024–2025.

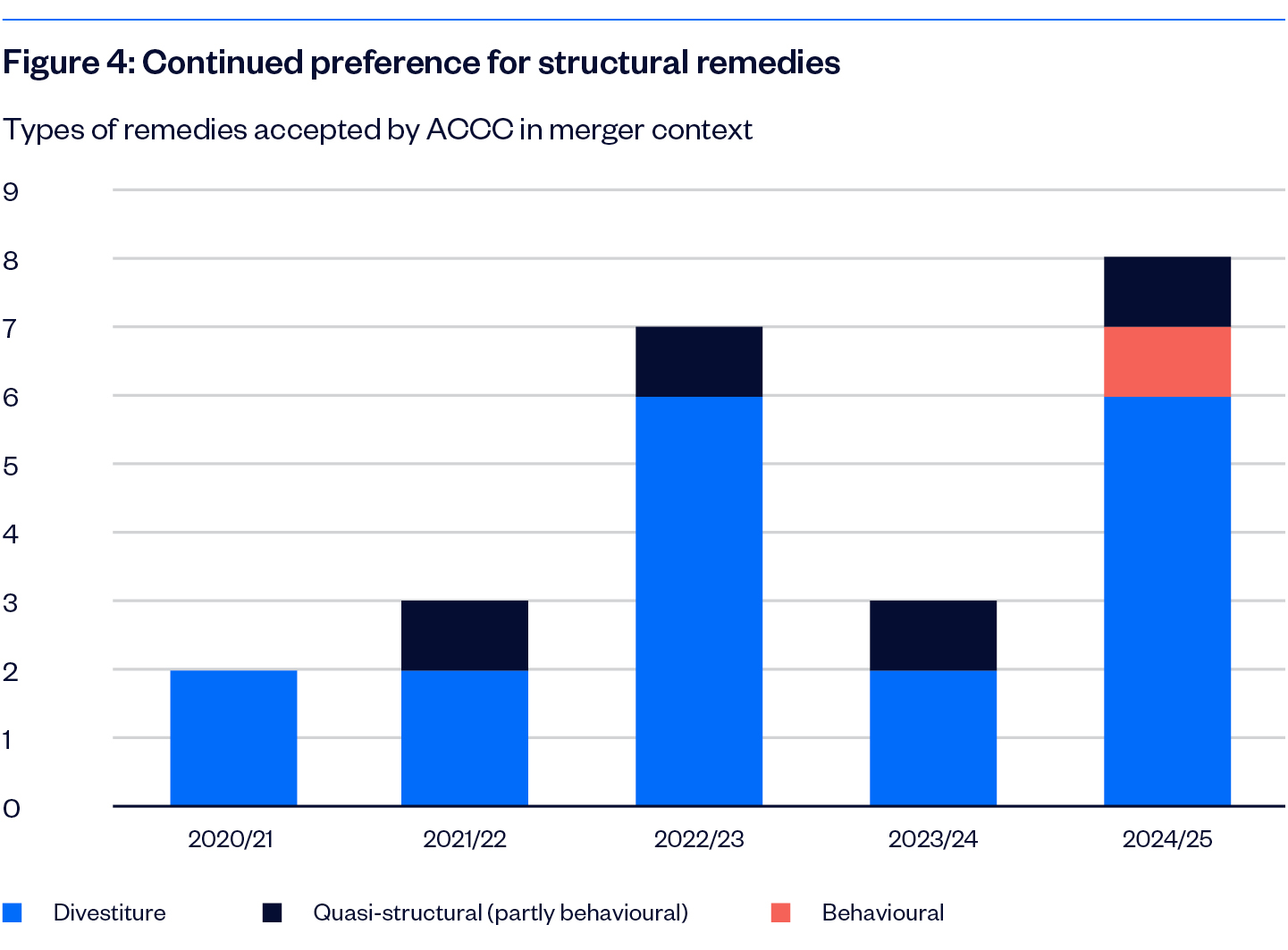

The ACCC continued preference for structural remedies

The ACCC continues to prefer structural remedies (i.e., divestment) to solve competition concerns created by transactions. This is consistent with antitrust regulators globally.

However, there has been some willingness to engage with quasi-structural and behavioural remedies in 2024-25 in two major and complex deals, both involving Gilbert + Tobin:

Sigma/Chemist Warehouse involved the highly-regulated pharmacy retailing and pharmaceutical wholesaling industries. In clearing the $9B deal, the ACCC accepted a set of remedies including a data protection remedy, a new termination right for Sigma’s franchisees and wholesale customers wishing to exit their agreements, and a commitment from Sigma to remain a participating wholesaler in the Commonwealth Government’s Community Service Obligation arrangements.

Qube/MIRRAT involved the acquisition of the Melbourne automotive import terminal by the existing national terminal operator, Qube. After a long and complex process, including multiple ‘red lights’, the ACCC accepted an undertaking which required Qube and MIRRAT to operate terminals on an open-access and non-discriminatory basis (replacing an existing undertaking at the Terminal).

Figure 4: Continued preference for structural remedies

Under the new merger regime, the ACCC has a new discretion to determine an appropriate remedy and is no longer confined only to accepting or rejecting commitments offered by the parties. It remains to be seen how the ACCC will exercise this power and what impact it may have on the ACCC’s willingness to impose remedies (including beyond those commitments offered by merger parties).

The new merger process also creates a more time-compressed and rigid framework for negotiating remedies, especially in complex transactions. Parties need to consider the question of remedies at an early stage if they want to avoid delays and, even then, it is not yet clear how ACCC engagement with remedies will work during Phase 1.

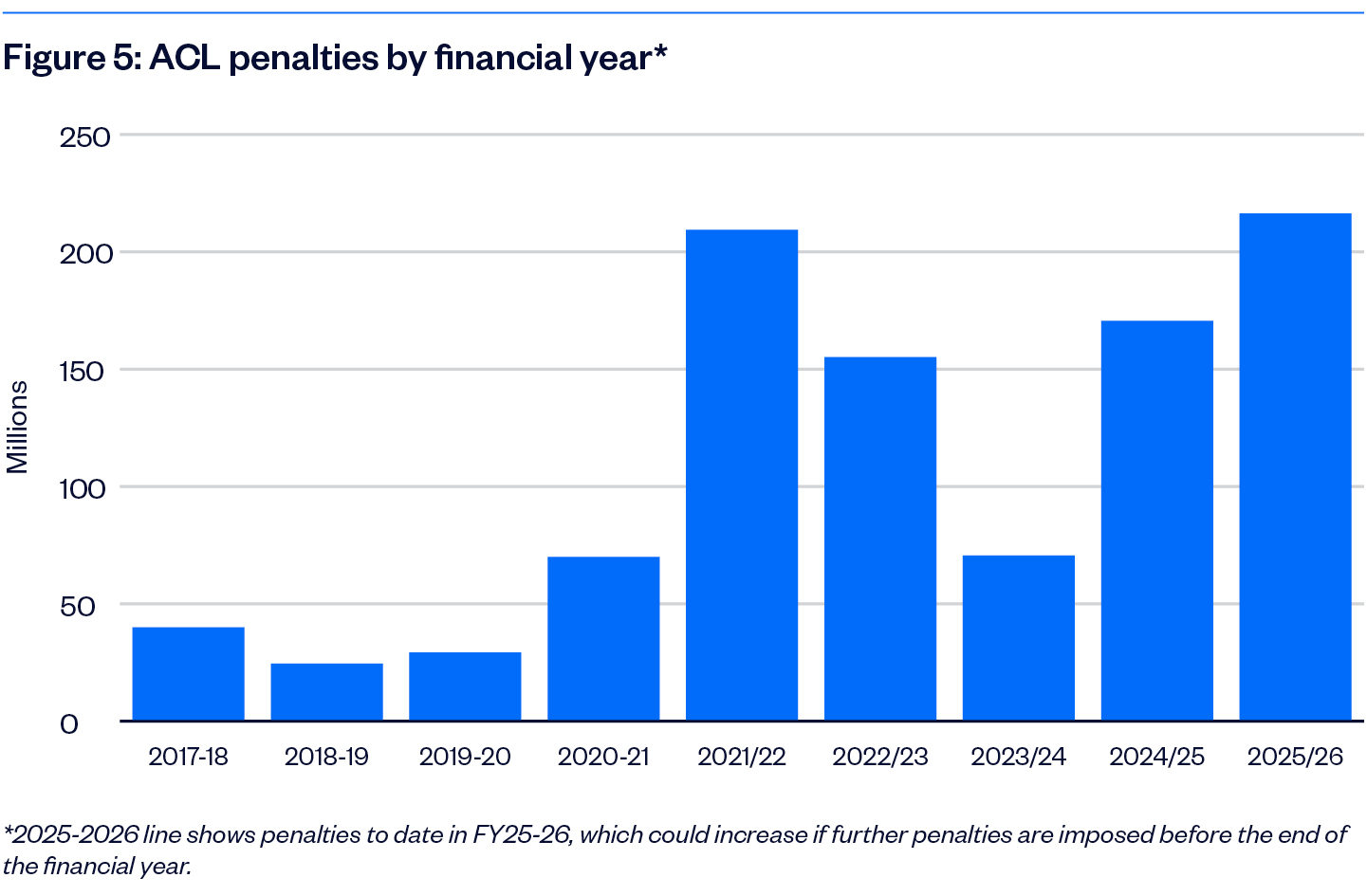

Consumer law penalties remain significant

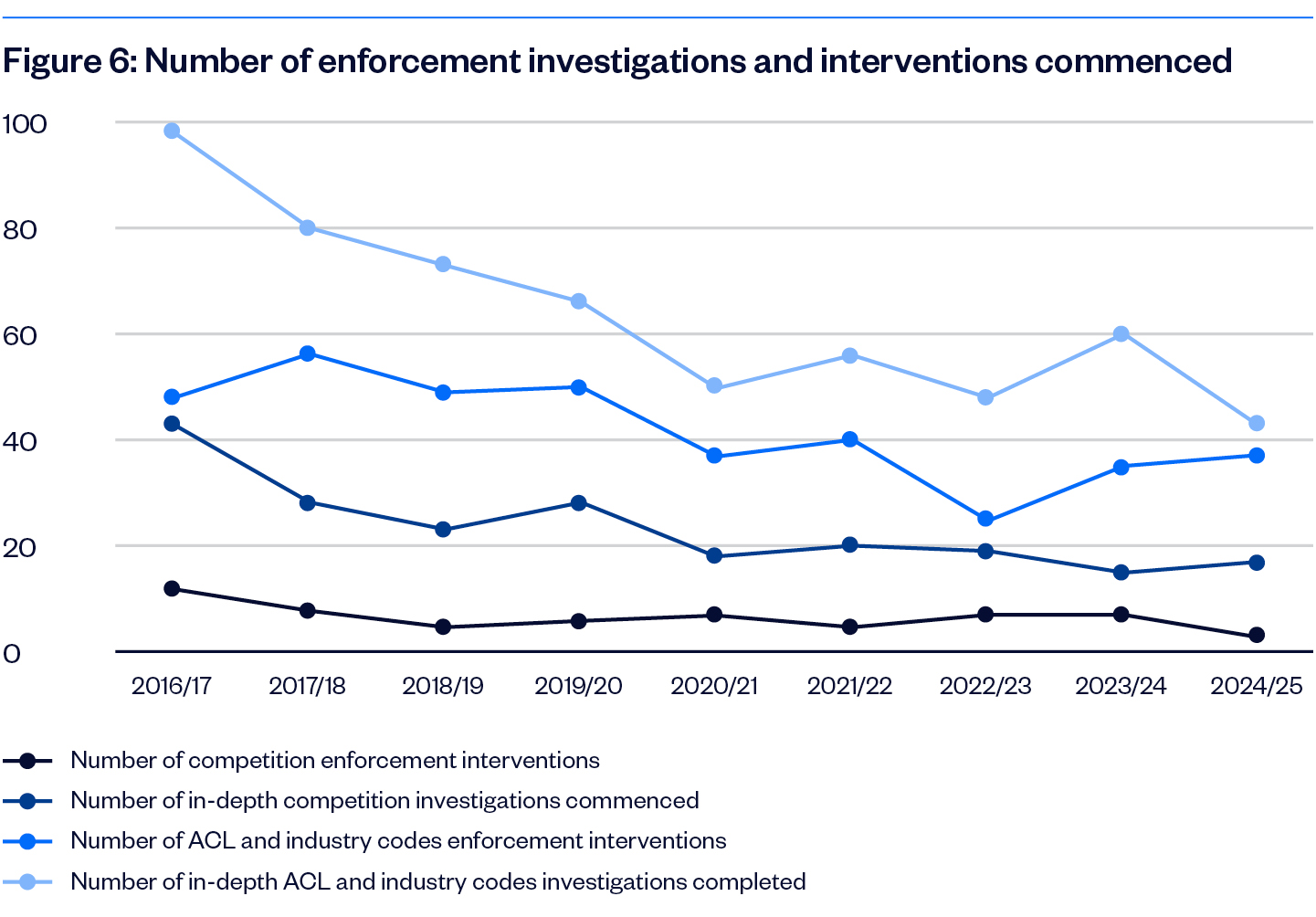

While the overall trend in the number of investigations commenced continued to fall (Figure 6), the ACCC targeted leading consumer brands and big fines in its consumer protection role during 2025 – with a particular focus on misleading conduct or alleged unconscionability (Figure 5).

Following the largest ever penalty under the Australian Consumer Law (ACL) when Qantas was ordered to pay $100 million in late 2024, the trend of significant penalties continued during the year as the ACCC pushes to ensure that penalties impose a direct and real deterrent.

Examples in 2025 included:

Optus paid $100 million for unconscionable conduct in selling mobile phones and contracts to consumers who did not want or need them and could not use or afford them.

Bupa paid $35 million for unconscionable conduct and misleading representations about its members’ health insurance entitlements.

Captain Cook College, Site Group and Blake Wills paid $30 million for unconscionable conduct towards students under the former VET FEE-HELP program.

Mosaic Brands paid $25 million for consumer law breaches including failing to deliver items to consumers within a reasonable time.

Telstra paid $18 million for migrating customers to new plans with lower maximum upload speeds.

City Beach paid $14 million for supplying non-compliant button battery products.

The Good Guys paid $13.5 million for misleading conduct in relation to its store credit promotions.

Webjet paid $9 million for false or misleading statements about the price of flights and booking confirmations.

Clorox paid $8.25 million for misleading claims about the use of ‘ocean plastics’ in certain GLAD products.

Figure 5: ACL penalties by financial year*

Figure 6: Number of enforcement investigations and interventions commenced

2025 may mark a subtle shift in the ACCC’s enforcement focus back to competition law

There was a slight increase in the number of in-depth competition investigations completed in 2024–2025: a total of 17 for the year, compared with 15 in 2023–2024.

After several years with reduced competition law litigation, the ACCC commenced three proceedings last year, one of which was commenced (with proposed remedies) by consent:

ACCC v Google: In August 2025, the ACCC commenced proceedings against Google Asia Pacific over anti-competitive understandings that Google admitted it had reached with Telstra and Optus in December 2019, regarding the pre-installation of Google Search on Android mobile devices. The matter was resolved between the parties before commencement of proceedings pursuant to a court-enforceable undertaking Google had provided to the ACCC.

ACCC v Veli Velisha Fresh Produce: In September 2025, the ACCC commenced proceedings against four suppliers and three senior executives for alleged price fixing while supplying fresh vegetables to ALDI between 2018 and 2024.

ACCC v Borger Crane Hire & Rigging Services: Also in September 2025, the ACCC commenced proceedings against four Sydney-based mobile crane hire companies and four senior executives for allegedly arranging not to supply services to certain customers or sites between 2020 and 2024. Two of the companies are also alleged to have fixed prices.

At the same time, in terms of investigative activity, there was a noticeable decline in 2024–2025 in the number of in-depth consumer law investigations completed: a total of 43 for the year, compared with 60 in 2023–2024.

Generally, competition law investigations are more costly, complex and resource-intensive for the ACCC than consumer law investigations – so it remains to be seen whether this marks a subtle but distinct return to investing greater internal attention and resources on competition enforcement.

The biggest competition litigation of the year was truly Epic

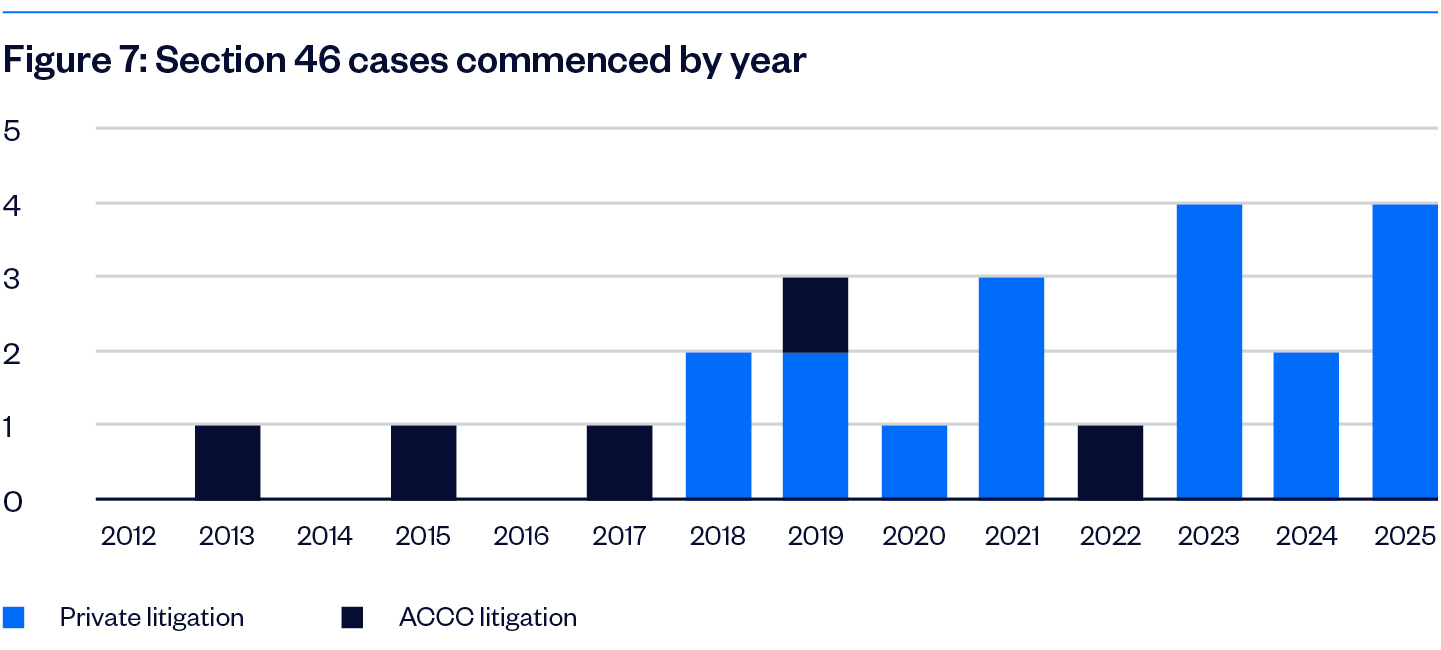

Australia’s unilateral market power was reframed in 2017 to introduce an ‘effects test’ and remove other perceived limitations on enforcement, in a move widely seen to lower the threshold for successful litigation.

Despite the ACCC having lobbied for the reforms, the changes did not result in an increase in cases commenced by the ACCC, which has brought only two cases under the new section, the most recent commenced in May 2022.

Instead, during 2025, private litigation continued to fill the void (Figure 7). Four new cases were brought by private litigants under section 46 during the year, including:

a further class action against Google in relation to its ad tech services (Riverine Grazier v Google)

new litigation against CSR by Consolidated Energy (formerly Australian Gypsum Industries), based on documents obtained in a previous litigation

litigation against Australia’s largest home improvement retailer (Woodman Beenleigh v Bunnings)

a now-settled litigation commenced by Employment Hero against SEEK Limited, Australia’s largest online jobs board.

Figure 7: Section 46 cases commenced by year

A range of other cases continue to work their way through the courts or have been settled or discontinued, suggesting that private section 46 litigation is increasingly being seen as a tool in commercial negotiations.

The Federal Court judgment in the series of Epic cases was the most significant, involving Epic’s claims against Apple and Google, as well as follow-on class actions (with conduct that largely reflected similar cases brought by Epic in the United States and raised with regulators in the EU).

Across three volumes and 2,000 pages, his Honour Justice Beach found that both Apple and Google had misused their market power by restricting the use of alternative app distribution methods and in-app payment methods on Apple or Android mobile devices. Similar findings were made in the two class actions. The case and judgment highlight the complexity and challenge of bringing misuse of market cases to trial.

The task will only get more complex as the next phase of the Epic saga turns to the determination of remedies in the first half of 2026. This will require Australian courts to wrestle for the first time with a number of complex questions involving the approach to damages and pricing in dominance cases. This will present an important precedent for a string of other section 46 cases involving pricing that remain before the courts.

Personnel changes at the ACCC

The year also saw changes in personnel at the ACCC.

Former Commissioner and head of the ACCC’s Enforcement Committee, Liza Carver, left the ACCC early in the year to return to private practice. She was replaced in July by her former partner and colleague Luke Woodward, who now heads up the same enforcement role. Commissioner Woodward is a seasoned competition litigator and it remains to be seen the extent to which his appointment may influence ACCC litigation focus and strategy in 2025.

Former Commissioner and Chair of the Digital ID and Consumer Data Right Committee, Peter Crone, completed his term in early December 2025. Dr Ian Opperman was appointed Commissioner at that time and now chairs that Committee. Commissioner Anna Brakey has also been reappointed to a second five-year term.

Competition law was again before the High Court

After disposing of the last of the air cargo cartel cases in 2017, the High Court was not called on to decide another competition law case until 2025 – when it was faced with two important cases.

In ACCC v J Hutchinson/CFMEU the High Court held that Hutchinson had not reached an arrangement or understanding simply because the CFMEU had threatened industrial action or conflict if Hutchinson continued to use a certain contractor and Hutchinson had acted as demanded.

This decision may have narrowed the scope for conduct to be considered an arrangement or understanding, though subsequent decisions by the Full Federal Court in ACCC v BlueScope and ACCC v Delta Building Automation suggest that an attempt to reach or induce an understanding may be more easily established, with both judgments affirming the lower courts’ findings of civil cartel conduct.

In Mayfield v NSW Ports, a private litigant, Mayfield, asked the High Court to reject the application of a finding of the Full Federal Court in ACCC v NSW Ports that NSW Ports was entitled to derivative crown immunity in the context of a privatisation, insofar as that finding applied to a proceeding commenced by Mayfield against NSW Ports.

Mayfield’s preliminary question was heard in the High Court in December 2025 and the ACCC was also granted leave to intervene in the proceedings. The decision could have a significant impact on arrangements between private parties and the government where there is sovereign risk.

Looking ahead to 2026

In addition to merger reform, the wider law reform agenda was also very busy in 2025 as competition and consumer policy were seen as a potential lever to improve productivity.

Changes you can expect to see in 2026:

Unfair trading practices: In February 2026, Treasury released draft legislation to introduce a general prohibition on ‘unfair trading practices’ that impact consumers. This will target conduct that unreasonably manipulates consumers or distorts their decision-making and causes detriment.

As well as the general prohibition, there will be specific laws targeting subscription traps and drip-pricing practices. Under the proposed reforms, businesses offering subscriptions in Australia would need to disclose key information before sign‑up, notify customers at critical points during a subscription, and provide a clear, straightforward way to cancel. Transaction fees would also have to be prominently disclosed.

The combination of a new ‘unfairness’ test with Australia’s existing and broad provisions governing both misleading or deceptive conduct, unconscionable conduct and unfair contracts, means that we will have one of the broadest general consumer protection standards globally. If the laws pass, they will commence on 1 July 2027.

Excessive pricing by major supermarkets: Treasury has also enacted new regulations which will ban ‘excessive pricing’ by major Australian supermarkets. The regulations apply from 1 July 2026 and target prices by Woolworths and Coles that significantly exceed the cost of supply plus a reasonable margin. ACCC Chair Gina Cass Gottlieb has publicly put the supermarkets on notice that they can expect enforcement action, as early as the second half of 2026.

Non-competes, no-poach, and wage fixing agreements: Consultation has also been completed on a proposed ban on non-compete clauses and separate stand-alone prohibitions for no-poach and wage-fixing agreements. Currently, most employment-related agreements are exempted from Australia’s cartel laws. The Government is considering its response, and we can expect to see draft legislation in 2026.

Improving price and loyalty program transparency in supermarkets: Treasury is consulting on proposed requirements for certain supermarkets to publish their prices online, ensure web‑scraping technologies can be used by third parties like online comparison websites and apps, display minimum information about promotions and provide timely information to members about loyalty programs. The initial consultation period on the policy and proposals is currently ongoing and draft legislation is yet to be released.

What does it all mean for 2026?

The pace and extent of change in Australia’s competition and consumer law landscape has been remarkable.

There is little indication that this will change or slow in 2026. Merger reform will continue to evolve as the ACCC and businesses work within the new regime. Competition enforcement appears on the rise and private section 46 litigation is being used more frequently in commercial disputes, alongside activist litigation and class actions.

These developments sit against a backdrop of the ACCC playing a significant role across the economy, with new and broadly defined prohibitions and, in some cases, coercive powers.

Australia’s new merger reforms have commenced and mark the most significant overhaul of Australia’s merger control framework in decades.