This publication explains some aspects of the rules governing foreign investment in Australia and the screening process.

Download the full report

Section 2: What laws govern foreign investment?

The main laws that regulate foreign investment in Australia are:

- The Foreign Acquisitions and Takeovers Act 1975 (Cth) (FATA) and the Foreign Acquisitions and Takeovers Regulation 2015 (FATR). Together these give the Australian Treasurer the power to review foreign investment proposals that meet certain criteria and to block such proposals that are contrary to the national interest (or national security, as applicable), or apply conditions to the way such proposals are implemented to ensure they are not contrary to the national interest (or national security, as applicable); and

- The Foreign Acquisitions and Takeovers Fees Imposition Act 2015 (Cth) and its associated regulations, which set the fees for applications.

Separate legislation imposes other requirements in respect of foreign ownership in certain industries. This brochure does not cover these industry-specific requirements.

Section 3: Some key foreign investment concepts

The following are important concepts in the legislation that help to determine whether someone is a foreign person (see section 4) or foreign government investor (see section 5) and whether an action is regulated by FATA (see section 6).

Corporations, trusts and incorporated limited partnerships

An interest of a specified percentage in a corporation, trust or unincorporated limited partnership includes the interests of a person’s associates and is measured slightly differently for each, but in general, it counts:

- for corporations and unit trusts, ownership interests and the ownership interests a person or its associates would hold if they exercised rights that they have (such as options);

- for unincorporated limited partnerships, rights to distributions of property; and

- in all cases, voting power and the voting power a person or its associates would hold if they exercised rights that they have (such as options).

In addition, for certain purposes under FATA, if a person has the power to veto any resolution of the board, central management or general meeting of a corporation, unit trust or unincorporated limited partnership, the person is deemed to have an interest of 20% or more.

In many cases, a person is taken to acquire an interest of a specified percentage if they already hold that percentage, and then increase it.

Businesses

An interest of a specified percentage in a business means the value of the interests in assets of the business held by the person and its associates versus the value of the total assets of the business.

Associates

As noted above, the interests that are counted include the interests of a person’s associates. The associates of a person (first person) include (among other things) the first person’s relatives; any person with whom the first person is acting in concert in relation to an action to which FATA applies; partners in a partnership; any entity of which the first person is a senior officer (and vice versa); and a corporation or trustee of a trust in which the first person holds an interest of 20% or more (and vice versa). These are subject to fairly narrow exceptions.

The concept of an interest of a specified percentage then feeds into the definitions of substantial interest, aggregate substantial interest and direct interest, which are used frequently in the legislation.

- A person holds a substantial interest if (in relation to a corporation, unit trust or unincorporated limited partnership) the person holds an interest of at least 20%, or if in relation to a trust, the person holds a beneficial interest in at least 20% of the income or property of the trust.

- The definition of aggregate substantial interest is similar, but it considers the holding of 2 or more persons, the threshold is 40%, and it does not apply to unincorporated limited partnerships.

- A direct interest includes:

- an interest of 10% or more in the entity or business;

- an interest of 5% or more in the entity or business if the person who acquires the interest has entered into a legal arrangement relating to the businesses of the person and the entity or business; and

- an interest of any percentage in the entity or business if the person who acquired the interest is in a position to influence or participate in the central management and control of the entity or business or to influence, participate in or determine the policy of the entity or business.

Do not be fooled by the terminology – a person can, by virtue of the application of the tracing rules (see section 3.3), acquire a direct interest indirectly.

Remember also that the ‘interest’ includes the interests of associates (see section 3.1).

Tracing rules operate up through chains of substantial interests, so that if a person has a substantial interest in a corporation, trust or unincorporated limited partnership (higher party), and the higher party has an interest of any percentage in a corporation, trust or unincorporated limited partnership (lower party), the person is taken to hold so much of the lower party as the higher party holds. This test operates through multiple chains of ownership and applies at each level irrespective of whether there is any practical control.

The legislation turns these tracing rules ‘on’ or ‘off’ for certain purposes, most notably in respect of offshore transactions (see sections 6.1 and 6.8).

Australian land includes commercial land, agricultural land, residential land and mining and production tenements. Interests include among other things:

- a freehold interest;

- a lease or license that is reasonably likely to exceed 5 years;

- an interest in an income or profit sharing venture relating to land (which includes royalty arrangements) that is reasonably likely to exceed 5 years; and

- an interest in a share or unit of an entity where Australian land makes up more than 50% of the assets of the entity.

Section 4: Who is regulated under foreign investment legislation?

The legislation generally regulates foreign investment proposals by a ‘foreign person’. A foreign person means:

- an individual not ordinarily resident in Australia;

- a corporation in which, or the trustee of a trust where in relation to the trust:

- an individual not ordinarily resident in Australia, a foreign corporation or a foreign government holds a substantial interest; or

- 2 or more persons, each of whom is an individual not ordinarily resident in Australia, a foreign corporation or a foreign government, hold an aggregate substantial interest;

- the general partner of a limited partnership where in relation to the limited partnership:

- an individual not ordinarily resident in Australia, a foreign corporation or a foreign government holds a substantial interest; or

- 2 or more persons, each of whom is an individual not ordinarily resident in Australia, a foreign corporation, or a foreign government, hold an interest of 40% or more; and

- a foreign government or foreign government investor (see section 5).

Section 5: Special rules for foreign government investors

Australia scrutinises a broader range of investments by ‘foreign government investors’ than it does investments by other foreign persons.

A ‘foreign government investor’ (FGI) includes:

- a foreign government;

- an individual, corporation or corporation sole that is an agency or instrumentality of a foreign country but is not part of the body politic of that foreign country (referred to below as a ‘separate government entity’); and

- a corporation, trustee of a trust or general partner of a limited partnership where in relation to the corporation, trust or limited partnership (1) a foreign government, separate government entity or FGI, together with its associates (including other FGIs from the same country), holds a 20% or more interest, or (2) FGIs, separate government entities or FGIs, together with their respective associates (including other FGIs from the same country), hold a 40% or more interest.

This definition is recursive so that it includes FGIs captured by prior applications and this paragraph.

The definition of FGI captures not only state-owned enterprises and sovereign wealth funds but also things like public sector pension funds, public universities, the investment funds into which state-owned enterprises, sovereign wealth funds, public sector pension funds and public universities invest and, due to tracing rules, portfolio companies for such investment funds.

While many investment funds will be deemed to be FGIs, an exception has been introduced specifically for them. Where:

- the investment fund is a scheme in which investors pool contributions to produce benefits;

- no individual member of the scheme is able to influence any individual investment decisions, or the management of any individual investments of the scheme (ie, no direct influence); and

- no individual member that is an FGI has any position in respect of the fund other than as a member of the scheme, the 40% test described above can be disregarded.

Funds may still benefit from this exception if investors have some influence over the broad investment strategy or are able to participate in collective decision making in relation to the fund, but are not involved in individual decisions about particular investments. Examples include:

- being on the advisory committee; and

- being able to influence the broad investment strategy of the fund, eg requiring the fund to divest from a particular sector, or to only make investments that meet ethical investing criteria.

For those funds that are still deemed to be FGI by virtue of the 20% test, a passive FGI exemption certificate can be applied for which has the effect that the fund will be treated as a private foreign person (rather than FGI).

Section 6: What type of foreign investment transactions are regulated under FATA?

There are four types of action which are regulated under FATA:

Significant actions

The Treasurer has the power to make orders in relation to these kinds of transactions (including to block them, impose conditions or to order divestments) if he or she considers the transaction to be contrary to the national interest. Significant actions only have to be notified if they are also notifiable actions or notifiable national security actions, but doing so and obtaining a notice of no objection cuts off the Treasurer’s powers including the call-in powers described in section 6.5, but subject to the last resort powers described in section 6.6. Once notified, a significant action cannot proceed until a notice of no objection is obtained.

Notifiable actions

These are a category of transactions which must be notified. Most notifiable actions are also significant actions.

Notifiable national security actions

The Treasurer has the power to make orders in relation to these kinds of transactions (including to block them, impose conditions or to order divestments) if he or she considers the transaction to be contrary to national security. These actions must be notified and cannot proceed until a notice of no objection is obtained.

Reviewable national security actions

These are transactions with an Australian nexus that are not significant actions, notifiable actions or notifiable national security actions. The Treasurer has the power to make orders in relation to these kind of transactions (including to block them, impose conditions or order divestments) if he or she considers the transaction to be contrary to national security. Like significant actions, reviewable national security actions do not have to be notified, but doing so and obtaining a notice of no objection cuts off the Treasurer’s powers including the call-in powers described in section 6.5, but subject to the last resort powers described in section 6.6. Once notified, a reviewable national security action cannot proceed until a notice of no objection is obtained.

The table in the guide sets out the key notifiable actions (all of which are also significant actions) for onshore transactions, as well as how the treatment differs (if at all) where the action is offshore (ie, indirect acquisitions).

From a practical perspective, significant actions that are not also notifiable actions include (among others):

- asset deals where the business being acquired is valued above the then current monetary threshold; and

- offshore acquisitions by private foreign investors (not involving land entities or media business), where the value of the Australian business is in excess of relevant monetary thresholds.

In general, the thresholds are the same as in the first row of the table in section 6.1.

A notifiable national security action includes any of the following actions by a foreign person:

- to start a national security business;

- to acquire a direct interest (as defined in section 3.2) in a national security business;

- to acquire a direct interest in an entity that carries on a national security business;

- to acquire an interest in Australian land that, at the time of acquisition, is national security land; and

- to acquire a legal or equitable interest in an exploration tenement in respect of Australian land that, at the time of acquisition, is national security land.

Note that there are no monetary thresholds, and the tracing rules can operate to capture offshore transactions. Further, offshore entities can carry on a national security business.

A national security business is one which is carried on wholly or partly in Australia (whether or not for profit) which is publicly known, or could be known upon making reasonable enquiries, to be one or more of the following:

- it is a responsible entity or direct interest holder of a critical infrastructure asset within the meaning of the Security of Critical Infrastructure Act 2018 (SOCI Act);

- it is a carrier or nominated carriage service provider to which the Telecommunications Act 1997 applies;

- it develops, manufactures or supplies critical goods or critical technology that are, or are intended to be, for a military use, or an intelligence use, by defence and intelligence personnel, the defence force of another country, or a foreign intelligence agency;

- it provides, or intends to provide, critical services to defence and intelligence personnel, the defence force of another country, or a foreign intelligence agency;

- it stores or has access to information that has a security classification;

- it stores or maintains personal information of defence and intelligence personnel collected by the Australian Defence Force, the Defence Department or an agency in the national intelligence community which, if accessed, could compromise Australia’s national security;

- it collects, as part of an arrangement with the Australian Defence Force, the Defence Department or an agency in the national intelligence community, personal information on defence and intelligence personnel which, if disclosed, could compromise Australia’s national security; or

- it stores, maintains or has access to personal information on defence and intelligence personnel which, if disclosed, could compromise Australia’s national security.

National security land is:

- certain defence premises;

- land in which the Commonwealth, as represented by an agency in the national intelligence community, has an interest that is publicly known or could be known upon the making of reasonable enquiries.

National security business and the SOCI Act

As noted above, one kind of national security business is the acquisition of a direct interest in a responsible entity or direct interest holder for a ‘critical infrastructure asset’, as defined in the SOCI Act. Critical infrastructure assets cover specified assets across 22 different sectors and include those assets which, if disrupted or compromised, could hamper the security or economic well-being of Australia.

Not all assets in these sectors are caught – the definitions are highly technical, and legal advice should be sought.

Could be known after reasonable enquiry

The definition of national security business includes businesses that are publicly known, or could be known after reasonable enquiry, to be of the specified kind. The government’s expectations as to the level of enquiry that potential acquirers will make are very high. As an example, in determining whether an asset like a data centre stores or has access to classified information, an acquirer will be expected to obtain advice on Australia’s Protective Security Policy Framework and follow the trails of breadcrumbs in it to determine whether the data centre stores classified information (the target’s views are not dispositive).

Carry on business in Australia

To be caught, an entity must carry on business in Australia. Importantly, this means offshore entities may carry on a national security business.

The definition of reviewable national security action is broad and complex, but the actions that will be most frequently caught are an acquisition of shares in a corporation that carries on an Australian business (or a holding entity of such a corporation), or units in an Australian unit trust (or a holding entity of such a unit trust), or an acquisition of assets in an Australian business, in each case which has the result that a foreign person:

- acquires, or will acquire, a direct interest in the entity or business; or

- will be in a position (or more of a position) to influence or participate in the central management and control of the entity or business; or

- will be in a position (or more of a position) to influence, participate in or determine the policy of the entity or business, where the action is not otherwise a significant action, a notifiable action or a notifiable national security action. Importantly, this kind of action can (through operation of the tracing rules) capture foreign corporations if they carry on business in Australia.

Other reviewable national security actions include entering into an agreement relating to the affairs of an entity, or altering a constituent document of an entity, as a result of which one or more senior officers of the entity will be under an obligation to act in accordance with the directions, instructions or wishes of a foreign person who holds a direct interest in the entity where the action is not otherwise a significant action, notifiable action or notifiable national security action. In these cases, the entity in question must generally be an Australian entity.

In respect of any reviewable national security action, or any significant action that is not a notifiable action or notifiable national security action and for which approval was not sought, the Treasurer retains the power for 10 years after the action is taken to “call in” the transaction for review if she or he considers that the transaction poses national security concerns. Notifying the transaction and obtaining a notice of no objection cuts off this power (subject to the last resort powers described in section 6.6).

Because of the breadth of transactions caught by this, the government has identified a number of categories of businesses in respect of which it encourages investors to seek advance approval (assuming the transaction is not otherwise a notifiable action or notifiable national security action). These include certain businesses in the following sectors:

- banking and financial services;

- communications;

- commercial construction contractors;

- commercial real estate;

- critical minerals;

- critical service providers and suppliers;

- critical technologies;

- defence providers;

- energy;

- health;

- education;

- information technology, data and the cloud;

- nuclear;

- space;

- gas;

- electricity; and

- ports.

The Treasurer can re-review actions notified after 1 January 2021 where approval has been given to determine whether a national security risk relating to the action exists, and if certain conditions are satisfied, the Treasurer may impose conditions, or vary or revoke any conditions that have been imposed, and may make orders prohibiting an action or requiring the undoing of a part or whole of an action. This includes, as a last resort, requiring divestment.

The conditions that need to be met before the Treasurer may exercise the last resort power are:

- Since the transaction was notified:

- the Treasurer has become aware that the applicant made a statement that was false or misleading in a material particular, or that omitted a matter or thing without which the statement was misleading in a material particular;

- the business, structure or organisation of the person has or the person’s activities have materially changed; or

- the circumstances in which the action was or is proposed to be taken have materially changed.

- The Treasurer conducts a review, receives and considers advice in relation to the action from an agency in the national intelligence community, takes reasonable steps to negotiate in good faith with the foreign person, and is satisfied that exercising those powers is reasonably necessary for purposes relating to eliminating or reducing the national security risk and that the use of other options under the existing regulatory systems of the Commonwealth, states and territories would not adequately reduce the national security risk.

- The Treasurer is reasonably satisfied that:

- the false or misleading statement or omission directly relates to the national security risk;

- the national security risk posed by the change of the business, structure or organisation of the foreign person or the change to the person’s activities could not have been reasonably foreseen or could have been reasonably foreseen but was only a remote possibility at the time of the original approval; or

- the relevant material change alters the nature of the national security risk posed at the time of the original approval.

- the false or misleading statement or omission directly relates to the national security risk;

Many private equity funds, and by extension their portfolio companies, will be deemed to be FGIs as a result of the application of these rules.

The analysis of whether a private equity fund is an FGI or not is done for each vehicle comprising a fund separately (not on a “whole of funds” basis).

If one vehicle comprising the fund is an FGI based on the 20% test described above (or the 40% test where the exemption described above cannot be relied upon), then its interest must be combined with that of its associates (1) for purposes of determining whether that vehicle requires approval and (2) for purposes of determining whether the underlying portfolio company becomes FGI. By way of example, suppose:

- Fund 1A has no FGI investors and is therefore not deemed to be FGI. It will acquire 91% of portfolio co (PC).

- Fund 1B has 20%+ US state pension fund money in it and is therefore deemed to be FGI. It will acquire 9% of PC. Ordinarily a 9% holding by itself (with no veto rights or board seats) would not be enough to require approval or to cause PC to be deemed to be an FGI.

- However, Fund 1A and Fund 1B are associates, as they are two vehicles comprising the same fund and therefore invest in lockstep and are managed by the

same manager. - Fund 1B (an FGI) together with its associate (Fund 1A) will be acquiring 100% of PC.

- Fund 1B therefore requires approval, and once acquired, PC will be deemed to be an FGI.

In making an application, a private equity fund manager should expect to provide detailed information about the ownership and control of the manager, as well as the investors in the various fund vehicles. With respect to information about investors, the manager will generally need to provide, for each fund vehicle that itself holds 5% or more of an applicant, the following information in relation to each investor that holds 5% or more of that vehicle:

- name

- type of entity (individual, corporation, foreign government, trustee and trust, general partner and unincorporated limited partnership)

- percentage interest held in the vehicle

- jurisdiction

- FGI status.

Investors may also be required to specify the following information:

- where FGIs from one country collectively hold more than 5% of the fund, the name, jurisdiction of organisation and percentage interest of each such FGI (regardless of how small the holding); and

- the aggregate ownership by FGIs, by country.

Note that FGI status is tested for each vehicle that comprises a fund, with association rules then “tainting” the rest of the fund, so purely structuring decisions can influence whether a fund is deemed to be FGI or not.

As noted in sections 3.3 and 6.1 above, the tracing rules can operate to capture offshore transactions. In summary:

- offshore transactions which, via the tracing rules, meet the requirements set out in section 6.1 will be captured as either significant actions or notifiable actions, as set out in that section – approval may be either required or advisable, depending on the circumstances, and advice should be sought;

- offshore transactions which, via the tracing rules, meet the requirements set out in section 6.3 will be captured as notifiable national security actions – approval is required; and

- offshore transactions which, via the tracing rules, meet the requirements set out in section 6.4 will be captured as reviewable national security actions – approval is advisable in certain circumstances, and advice should be sought.

Section 7: National interest and national security tests

In determining whether a foreign investment proposal is contrary to the national interest, the Treasurer is able to examine any factors that he or she considers appropriate. Typically, these factors include the impact of the foreign investment proposal on:

- national security;

- data security;

- competition (noting that this is a different test to the test applied by the Australian Competition and Consumer Commission in examining merger clearances);

- the economy and the community (such as the investor’s plans to restructure the business in Australia after the acquisition);

- other government policies such as tax and the environment; and

- particularly where an investment is made by a foreign government investor, the Treasurer will also consider the character of the investor.

Some kinds of foreign investment proposals give rise to more specific concerns, which the Australian government takes into consideration (in addition to those described above) when examining those proposals:

- for agricultural investment proposals, the Australian government typically considers the effect of the proposal on the quality and availability of Australia’s agricultural resources, including water; land access and use; agricultural production and productivity; Australia’s capacity to remain a reliable supplier of agricultural production, both to the Australian community and Australia’s trading partners; biodiversity; and employment and prosperity in Australia’s local and regional communities;

- for residential real estate investment proposals, the overarching principle is that the proposal should increase Australia’s housing stock (by creating at least one new additional dwelling); and

- where a foreign investment proposal involves a foreign government investor, the Australian government considers if the proposed investment is commercial in nature or if the investor may be pursuing broader political or strategic objectives that may be contrary to Australia’s national interest.

Notifiable national security actions and reviewable national security actions are reviewed against a narrower “national security” test. There is no particular definition of national security, or what may pose a national security risk. FIRB generally considers whether a particular sector might be a target for espionage, sabotage or foreign interference and the magnitude of disruption that such activities could cause.

Section 8: Penalties and offences

It is an offence punishable by 10 years imprisonment or a monetary penalty1 for a foreign person to:

- take a notifiable action or notifiable national security action without having first obtained a no objection notification from the Treasurer; or

- take a significant action that the person has notified to the Treasurer but has not yet obtained a no objection notification for.

The same penalty applies if a person breaches a condition contained in a no objection notification or an exemption certificate.

The FATA also contains significant civil penalties for certain breaches . The maximum civil penalty for breaches such as failure to give notice to the Treasurer before taking a notifiable action, taking a significant action in certain circumstances without having first obtained a no objection notification, or breaching conditions contained in a no objection notification, is the lesser of:

- 2,500,000 penalty units ($825 million); or

- the greater of the following:

- 5,000 penalty units ($1.65 million) (or 50,000 penalty units ($16.5 million) if the person is a corporation);

- an amount determined by reference to the consideration or market value for the action.

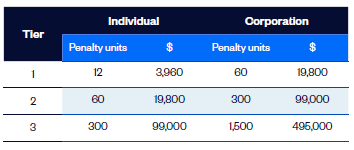

The FATA also contains a 3-tier infringement notice regime for contraventions of FATA which applies as follows:

- tier 1 penalties apply if the person self-discloses an alleged contravention of the FATA before the person is notified by the Commonwealth that the conduct is being investigated;

- tier 2 applies in all other cases, except (generally) for high-value acquisitions that are captured by tier 3; and

- tier 3 for non-compliance in relation to high-value acquisitions (i.e. above $5 million for acquisitions of residential land or above $275 million in other instances).

The penalties that can be issued under the infringement notice regime are set out in the table below.

Section 9: What's new for 2026?

- The government is making attempts to simplify and streamline the foreign investment legislation and the approval process, while at the same time ramping up compliance and holding foreign investors who breach the foreign investment legislation to account.

- On the compliance front, the Treasurer launched its first proceedings against a foreign investor for breach of a disposal order and was successful. In 2023 the Treasurer blocked an attempt by Yuxiao Fund (controlled by a Chinese businessman) to increase its stake in Northern Minerals Ltd. After an investigation into share trading, in June 2024, the Treasurer ordered five investors with apparent links to China, including Indian Ocean International Shipping and Service Company Ltd, to divest their stake in Northern Minerals to unconnected persons. Indian Ocean then transferred its shares in Northern Minerals to its director and sole shareholder (who subsequently divested her stake in Indian Ocean and resigned as director). In July 2025, the Treasurer brought action for failure to comply with his disposal orders. In January 2026, the court held that the transfer of shares breached the disposal order and imposed A$14m in civil penalties against Indian Ocean and its former shareholder / director.

- The government has also increasingly been willing to issue infringement notices, including Tier 3 infringement notices, for breach of the foreign investment laws. Breaches of the rules are then taken into account in assessing the character of a foreign investor, which forms part of the national interest test.

- Treasury has also become more strict regarding the provision of information. As most people familiar with the application process would be aware, the government assesses every application on the basis of the who, the what and the how, and the identity of investors in private equity funds is an important component of the "who". The government has been more consistent in requiring investors to provide detailed information about investors in private equity funds - please see section 6.7 for further details.

- The new foreign investment portal has proved challenging for more complex transactions, including transactions by private equity funds with complex structures. In response to law firms' creative attempts to provide information that did not fit well within the portal, Parliament passed a new law in December 2025 which permits the Treasury to reject an application where required information is not provided in the required way. It remains to be seen how often this power is used.

- The government undertook a consultation at the end of 2025 relating to a new tranche of foreign investment reforms. Key areas for discussion were further streamlining efforts (including a potential new streamlined notification regime for non-sensitive transactions that are caught by the legislation but which the government perceives would not ordinarily require detailed review; reform of the Register of Foreign Ownership of Australian Assets, which many agree is completely broken; enhancing the government's enforcement powers around avoidance-type behaviours (currently the government has limited powers around avoidance and there are no civil or criminal penalties for avoidance); and further technical fixes to the legislation.

This brochure explains some aspects of the rules governing foreign investment in Australia and the screening process. This information is current as of 1 April 2026. Australia’s foreign investment rules are complex, and this brochure is not exhaustive. This publication is for information purposes only and does not constitute legal advice. If you want legal advice, you must seek specific advice tailored to your circumstances, and you should not rely on this publication as a substitute for obtaining legal advice. The content is general information only, and Gilbert + Tobin cannot be held responsible for any liability whatsoever or for any loss or damage howsoever arising from or in reliance upon the whole or any part of the contents of this document. This publication may not be reproduced, distributed or transmitted in any form or in any manner, in part or as a whole without the prior written permission consent of Gilbert + Tobin. © Gilbert + Tobin 2026.