Businesses and the Australian Competition and Consumer Commission (ACCC) are adjusting to the new mandatory merger control regime. We observe the ACCC has been working hard to implement and ensure the effectiveness of the new regime as the primary administrative decision-maker, including consistently developing and evolving its internal processes to meet its statutory obligations. At the same time, businesses are familiarising themselves with the new regime, with a number of non-complex transactions having worked their way through the process from start to finish and the first complex transactions slated to conclude in the next month.

Key learnings from the early days of the new regime are:

- Frequent use of waivers in appropriate cases. Merger parties have been taking advantage of the fast-tracked waiver process, with over half (72) of the 136 applications to date being processed as waivers. These waiver applications have been dealt with relatively quickly by the ACCC, with a median processing time of 12 business days for the waivers that were determined and published during the first quarter. Nevertheless, the ACCC has also rejected six waiver applications during the first quarter. Given risks around transactions becoming ‘void’ and the uncertainty of exemptions, waivers are also being sought for a range of conduct outside of standard asset deals, such as strategic outsourcing arrangements. The ACCC has continued to adapt and update its waiver guidance to ensure only the most straightforward transactions are filed for waiver.

- Overall review timing is impacted by pre-notification engagement. The ACCC has met its own internal KPIs for timeframes for decision-making, with over 90% of applications being decided within 20 business days of notification against an internal target of 80%. These statistics include waivers and do not take into account pre-notification engagement periods. Based on transactions Gilbert + Tobin has worked on, pre-notification is taking an average of 3 weeks and in some cases up to more than two months. The ACCC has said that future reporting will include details of pre-notification timing, which is an important area of focus given the impact it has on overall engagement timelines. In complex deals, this pre-engagement stage can include multiple rounds of requests for information and obtaining market feedback.

- Extensive information requirements. In G+T’s experience, the ACCC has been strict in its approach to information requirements under the new regime. In respect of waivers, the ACCC’s focus has been on market share information and disclosures in respect of the activities of connected entities in the context of portfolio groups, such as private equity firms. For full notifications, the notification forms are operating as a starting point for the information required by the ACCC in pre-notification, before the review commences. The ACCC has typically issued informal requests for information and, in some cases, compulsory information notices during pre-notification engagement, with these requests not being limited to the information specified in the notification form. We have also seen the ACCC commence targeted market inquiries with key stakeholders in the pre-notification phase.

- The timing and process for negotiating remedies are challenging. As expected, early experience with remedies suggests that the process is more rigid and timing challenges arise, particularly if there is a desire to negotiate remedies during Phase 1.

- ACCC conditions precedent are evolving. The new process has changed a number of features of CPs. This includes sellers taking a more active role in understanding and managing the ACCC risk and process, which is often reflected in regulatory cooperation provisions. The substantial size of Phase 2 filing fees means that many buyers, in smaller transactions, are looking for an “off ramp” through the ACCC CP to exit transactions in circumstances where the ACCC pushes a deal into Phase 2.

- Some little frustrations remain to be ironed out. The process continues to evolve and improvements continue. Clients need to be prepared for a number of small, process steps that can require additional time and have posed frustration, including the process around payment of filing fees (which cannot be paid until after a notification has been filed), some limitations with the ACCC portal and the need to wait two weeks after a notification is accepted before completion. Work continues with Treasury and the ACCC to iron these out.

- ACCC has been scrutinising pre-completion integration terms and non-competes. Under the new regime, parties must not put an acquisition into effect until after clearance has been obtained. This places additional scrutiny around the extent of pre-completion integration activities undertaken by the parties. In our experience to date, the ACCC has looked carefully at these provisions. The ACCC also has new powers to disallow non-competes in business sale agreements which extend beyond what is reasonably necessary to protect the position of the buyer. The ACCC has also been scrutinising these carefully.

Below are key statistics and our analysis of the new merger regime and the ACCC’s role in the first three months since the regime became mandatory on 1 January 2026.

Number of notifications and waivers

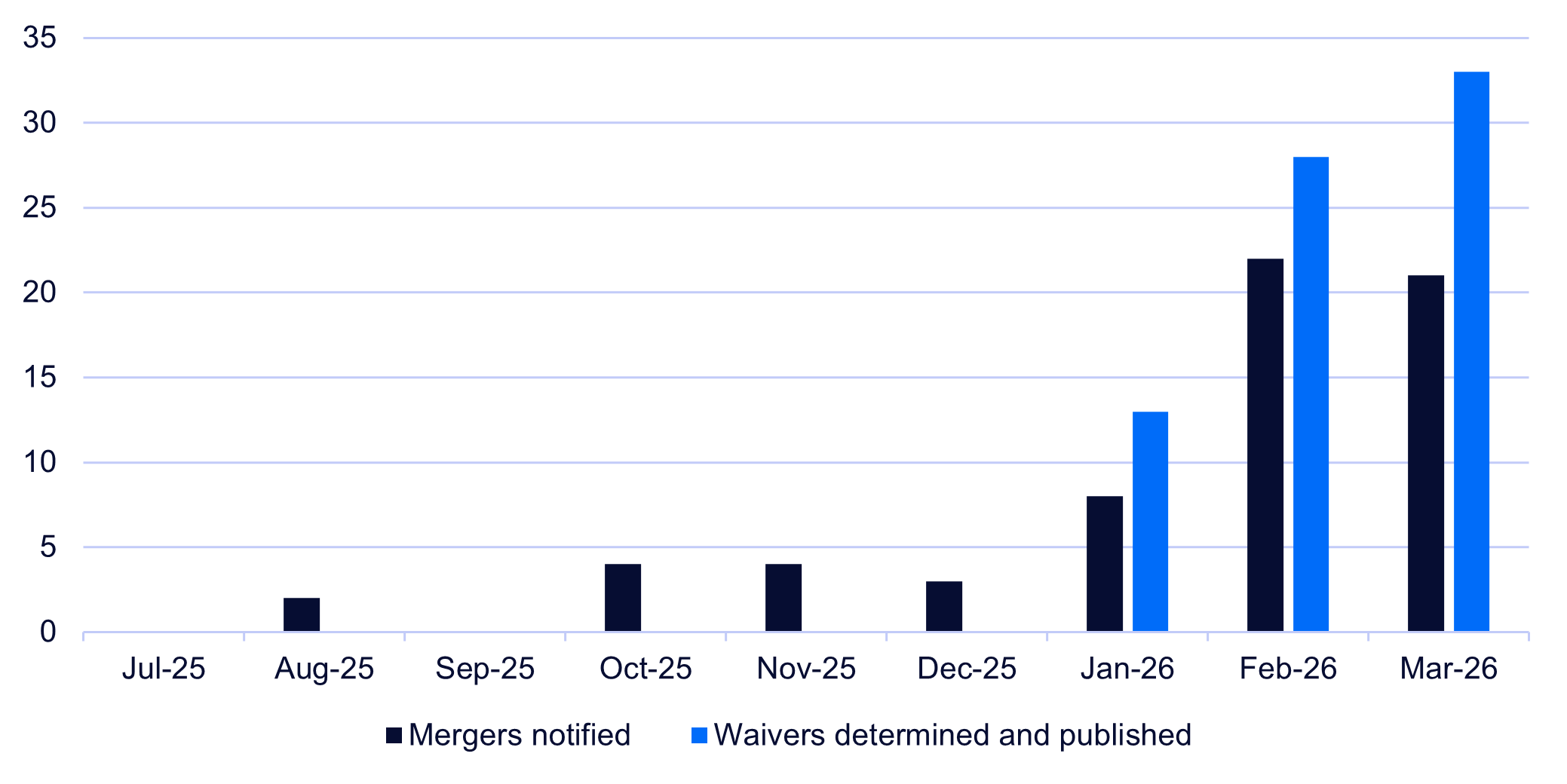

In the first three months since the new merger review regime became mandatory on 1 January 2026, 50 merger notifications were lodged (as compared with 13 in July 2025 to December 2025 when the regime was voluntary) and 108 waiver applications were received with 71 of those determined, as the ACCC has noted.

Below is a graph illustrating the increase in the number of mergers notified and increase in waivers determined by the ACCC, on a monthly basis. This includes the merger notifications received during the transitional period between 1 July and 31 December 2025 when voluntary notifications became available. As shown below, since the new regime commenced on 1 January 2026, there has been:

- a significant up-tick in the number of mergers notified; and

- an increase in the number of waivers determined by the ACCC..

Number of mergers notified and waivers determined, by month

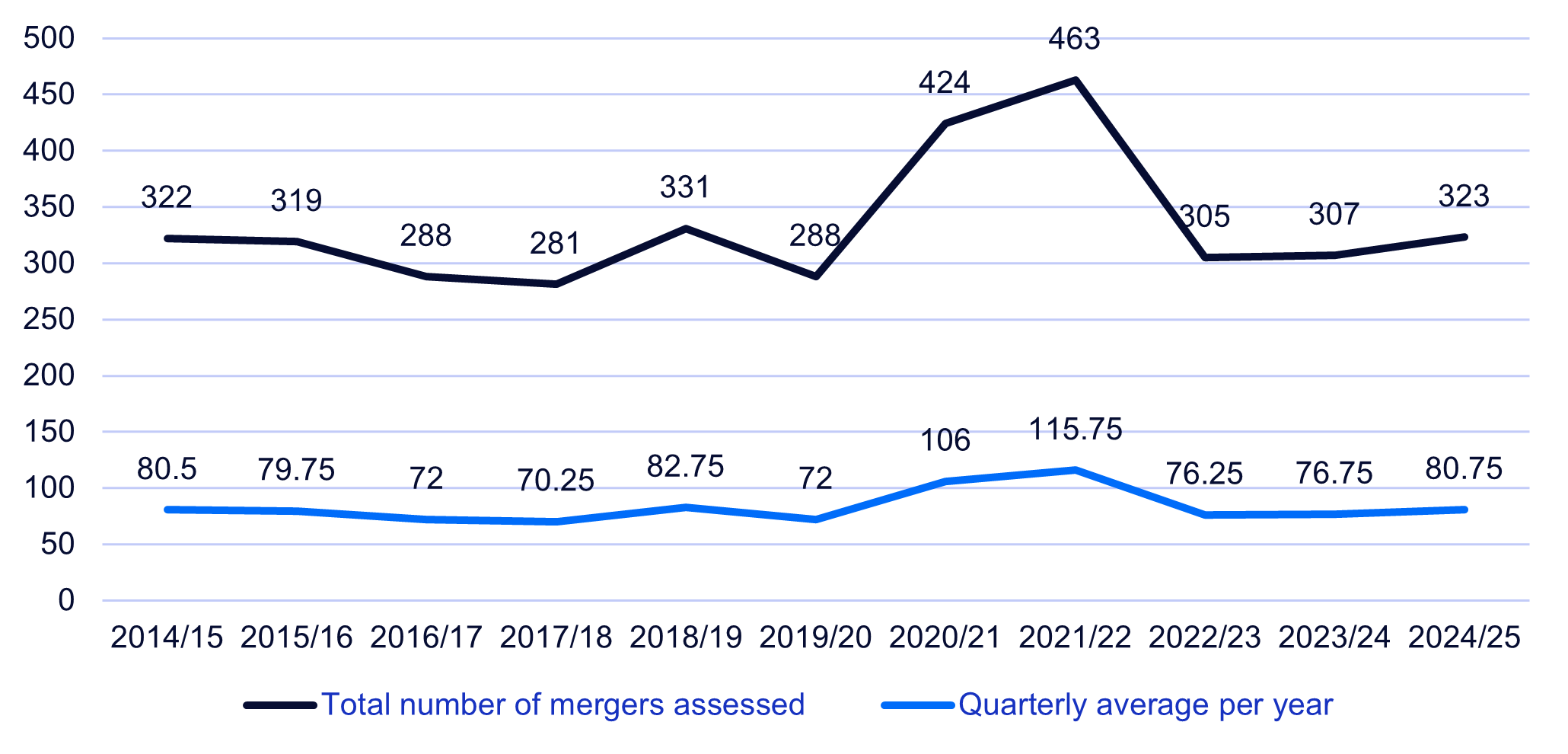

Compared with the prior voluntary regime and as shown in the graph below, the total number of waiver applications and merger notifications received in the first quarter (158) has already surpassed:

- half of the total number of mergers assessed by the ACCC the past three years;

- a quarter of the yearly number of mergers notified to the ACCC each year over the past decade.

Number of mergers assessed by the ACCC under the prior voluntary merger regime

Outcomes and timeframes for notifications

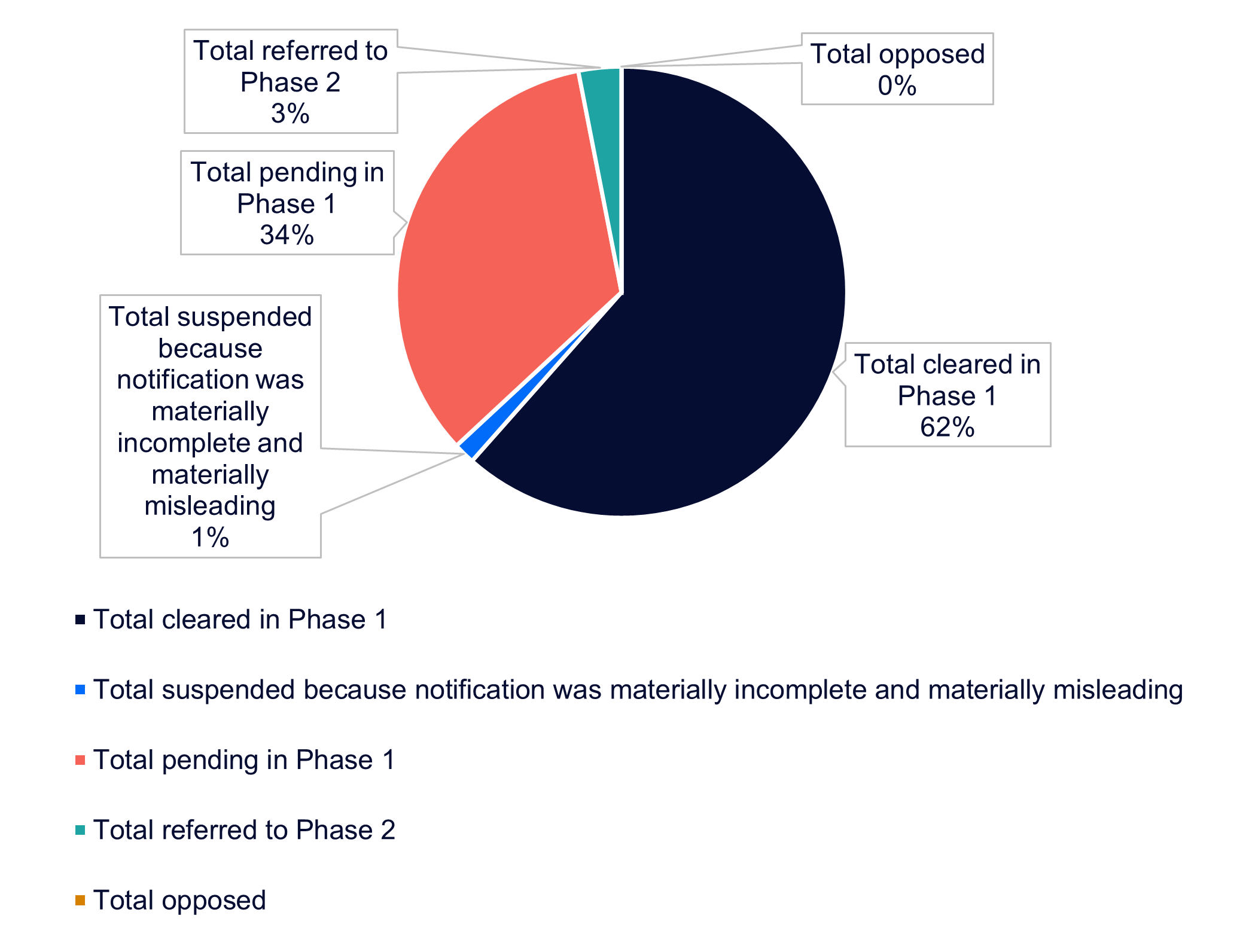

During the merger reform consultation process, the ACCC said it expects about 80% of mergers to be cleared within 15 to 20 business days. The ACCC also said it expects to be able to identify and raise any issues material to its Phase 1 assessment with the notifying party, including those raised by third parties, as soon as practicable and generally no later than Business Day 18 (ACCC merger process guidelines, December 2025, paragraph 6.21).

Of the 64 notified mergers so far (including voluntary and mandatory notifications from 1 July 2025 to 31 March 2026 but excluding waiver applications):

- 62.5% (40) have been cleared in Phase 1, at an average of 20 business days and a median of 17 business days.

- 1.5% (1) review was suspended because the ACCC considered the notification was “materially incomplete and materially misleading” (Sembcorp Industries Ltd - Alinta Energy). The ACCC has since recommenced its review following receipt of additional information and documents from Sembcorp.

- 3.1% (2) have been referred to Phase 2, neither of which has resulted in an outcome yet. So far, these two mergers have taken an average of 46.5 business days for Phase 1 review. Subsequent to this reporting period, a further two notifications have been referred to Phase 2. On 2 April 2026, the ACCC referred a third matter to Phase 2 after it had been reviewed in Phase 1 for 28 business days, and on 16 April 2026, the ACCC referred a fourth matter to Phase 2 after it had been reviewed in Phase 1 for 30 business days.

- None have been opposed or referred to the Public Benefits Phase.

Outcome of merger notifications (1 July 2025 to 31 March 2026)

Analysis of mergers that have proceeded to Phase 2

Of the four mergers that have proceeded to Phase 2 since the new regime commenced (two of which were referred within the first quarter):

- One involves the proposed acquisition of retail fuel sites (Ampol – EG Australia).

- Another involves the proposed acquisition by a supermarket of a leasehold interest in a new neighbourhood centre (Coles – supermarket and liquor site in Kalgoorlie, WA).

- The third, referred to Phase 2 on 1 April 2026, involves the proposed acquisition of kegs and certain assets (MicroStar Logistics – Konvoy) – the ACCC had previously opposed this transaction under the old informal merger review regime.

- Similarly, under the prior informal clearance regime, the ACCC had opposed the proposed acquisition of 100% of the issued share capital in RAC Insurance (RACI) from RACI Pty Ltd, a wholly owned subsidiary of the Royal Automobile Club of Western Australia Inc, by Insurance Australia Group (IAG). The parties then applied under the new regime and the ACCC has referred the matter to Phase 2 on 16 April 2026.

In both the Ampol – EG Australia and Coles – supermarket and liquor site in Kalgoorlie, WA matters, the ACCC published a Summary of Notice of Competition Concerns (NOCC) which provides insight into how the ACCC applies economic concepts to the new merger regime. In relation to MicroStar Logistics – Konvoy, and IAG - RACI so far the ACCC has published decision documents explaining why the acquisitions are subject to a Phase 2 review. Below is a table summarising concerns raised by the ACCC in these documents.

Document | ACCC’s preliminary views | Market concentration | Unilateral effects | Create, strengthen and entrench (CSE) a substantial degree of market power | Other interesting points |

| NOCC for Ampol – EG Australia, 2 March 2026 | The Acquisition would have the effect or be likely to have the effect of SLC in: (1) 51 local markets where 54 EG Australia sites overlap with Ampol sites; and (2) the retail supply of fuel in the metropolitan markets of Brisbane, Melbourne, Sydney and Canberra. | In some local areas, the post-acquisition site share is as high as 75% and the increment is as high as 50%. The ACCC is also considering the distance between the Ampol and EG Australia sites, and the number, identity and location of remaining competitors. | As for the retail supply of fuel in Brisbane, Melbourne and Sydney, the ACCC’s preliminary view is that the removal of EG Australia would likely lead to a SLC through unilateral effects because the Acquisition: (1) removes a direct and significant competitor to Ampol and other major fuel retailers, (2) increases Ampol’s share of sites in each of these three metropolitan markets and (3) may result in higher prices for consumers as Ampol would implement its own pricing strategies to the EG Australia network. | N/A | The ACCC is also considering a divestiture undertaking proposed by Ampol – this is the first remedy offer considered by the ACCC under the new merger regime, noting that remedies can only be offered within certain timeframes. |

NOCC for Coles – supermarket and liquor site in Kalgoorlie, WA, 5 March 2026 | The Acquisition would have the effect or be likely to have the effect of SLC in the retail supply of groceries by supermarkets in Kalgoorlie. | The ACCC referred to its Supermarkets Inquiry, in which it considered the Australian supermarket industry is generally highly concentrated and that Coles and Woolworths have limited incentive to compete vigorously on price. | N/A | This is the first matter in which the ACCC has applied this concept. Specifically, the ACCC considers that the Acquisition leads to the exit of an effective independent competitor and increases Coles’ market power, which would be likely to, in all the circumstances, CSE a substantial degree of market power for Coles. | The ACCC considers that the Acquisition will likely create an over-supply of supermarket capacity and thereby lead to the exit of an effective independent competitor. This will: (1) reduce the level of competition faced by remaining rivals, in circumstances where the likelihood of new entry is low and (2) increase Coles’ market power such that Coles would likely have a substantial degree of market power. |

Decision to subject MicroStar Logistics – Konvoy to Phase 2 review, 1 April 2026 | The Acquisition could have the effect, or likely effect, of SLC in the supply of keg pooling services in Australia by removing Konvoy as an effective competitor to MicroStar. | N/A – the ACCC simply considers that post-Acquisition, MicroStar would not face significant competitive constraint because its closest competitor would be removed from the market. | N/A | N/A | This is the parties’ second attempt at ACCC clearance for this deal, which was opposed in October 2025 under the previous informal regime. Information before the ACCC indicates that customer countervailing power would be unlikely to sufficiently constrain MicroStar, and there appears to be a low likelihood of timely new entry or expansion at sufficient scale to replace the loss of constraint due to the Acquisition. |

Decision to subject IAG – RACI to Phase 2 review, 16 April 2026 | The Acquisition could have the effect, or be likely to have the effect, of substantially lessening competition in both the supply of motor vehicle insurance and the supply of home and contents insurance in Western Australia. | The ACCC considers that the acquisition would combine two of the biggest insurers in WA (noting RACI is WA’s market leader both in motor vehicle insurance and in home and contents insurance). | N/A | N/A | N/A |

Outcomes and timeframes for waiver applications

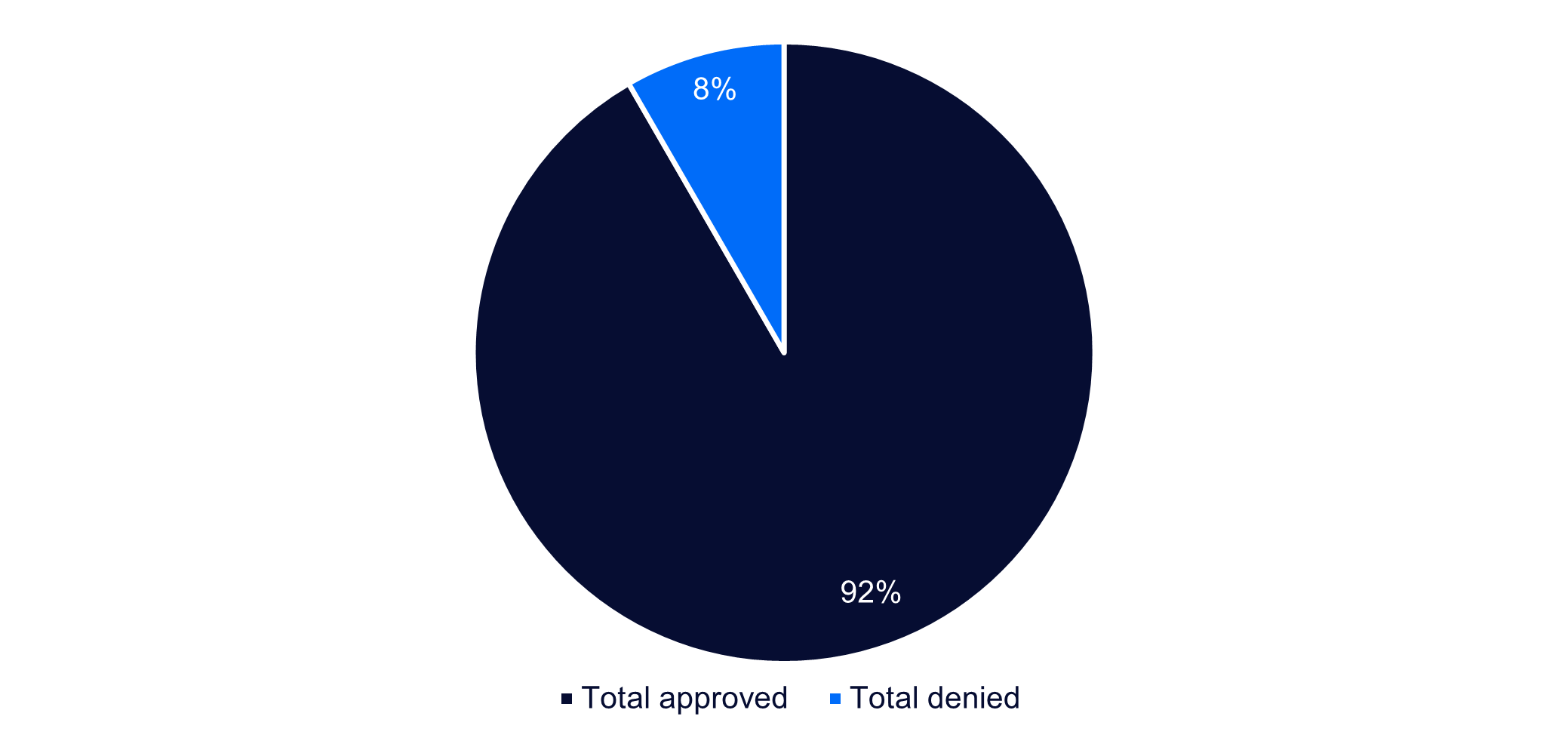

As shown below, of 72 waiver determinations in January to March 2026, 92% were approved and 8% were denied.

Outcome of waiver applications, Q1 2026

Below is a table summarising the six waiver applications that were denied in the first quarter of 2026, all of which involve different industries.

The ACCC considered that, if each of the acquisitions below were put into effect, the notification thresholds would be met. The ACCC also expressed varying degrees of concerns about competition issues, noting that typically at least two of the merger factors below were identified by the ACCC in its reasons.

Waiver application | Industry | Degree of ACCC competition concerns | Whether ACCC considers either party is the leading provider | Vertical relationships | Horizontal overlaps | Dynamic markets |

| Salesforce – Qualified | Computer system design and related services | The ACCC considered that the Acquisition may raise competition issues. | Yes – the ACCC considers that Salesforce is the leading provider of CRM software to businesses in Australia and is significantly larger than the next largest supplier. | Yes – the ACCC considers there is a vertical relationship between the products supplied by the merger parties. | N/A | Yes – the ACCC considers that the parties operate in complex and dynamic markets, including the provision of agentic AI. |

Accommodation and travel | The ACCC was unable to reach a view that the Acquisition would not be likely to raise competition issues in any market based on the information provided. | Not quite. So far, the ACCC has only said it may focus on the extent to which the parties are likely to face competition from alternative suppliers at these locations, particularly in relation to Maria Island, where alternatives appear limited. | N/A | Yes – the ACCC said it may focus on the extent of any horizontal overlap between Intrepid Travel and Wild Bush Luxury in the supply of tourism services in Australia, and particularly in Maria Island, the Top End and Flinders Ranges. | N/A | |

Cleaning and adhesive manufacturing, financial asset manufacturing | The ACCC was unable to reach a view that the Acquisition would not be likely to raise competition issues in any market based on the information provided. | No – the ACCC was silent on this. | Yes – the ACCC said it may focus on the vertical relationship between the products supplied by Henkel and ATP and the likely impact of the Acquisition on the parties’ ability and/or incentive to foreclose rivals. | Yes – the ACCC said it may focus on the extent of any horizontal overlap between Henkel and ATP in the supply of PSA tapes in Australia. | N/A | |

Human pharmaceutical and medicinal product manufacturing, scientific research services | The ACCC considered that the Acquisition may raise competition issues. | Not quite. So far, the ACCC has only said it may focus on the extent to which the Acquisition would remove potential competition from either party, as well as the extent to which the parties are likely to face competition from alternative suppliers. | Yes – the ACCC said it may focus on the nature and extent of any vertical or conglomerate relationship between the parties and their ability and/or incentive to engage in exclusionary conduct, bundling or tying of products post-Acquisition. | N/A | N/A | |

Fruit and vegetable growing, processing, wholesaling, retailing and packaging | The ACCC was unable to reach a view that the Acquisition would not be likely to raise competition issues in any market based on the information provided. | Not quite. The ACCC said it may focus on the potential for foreclosure, noting that Premier Fresh is one of the largest horticultural wholesalers. | N/A | Yes – the ACCC said it may focus on the extent of horizontal competitive overlap and the nature of the vertical relationship between Premier Fresh and the Domenico Group in the production and supply of capsicums in Australia which is unclear based on the application. | N/A | |

Water freight transport and other water transport support services | The ACCC was unable to reach a view that the Acquisition would not be likely to raise competition issues in any market based on the information provided. | No – the ACCC was silent on this. | N/A | Yes – the ACCC said it may focus on the extent of any potential horizontal overlap and/or complementary relationship between PT Asian Bulk Logistics (including its subsidiaries) and Engage Marine in the supply of marine services, transhipment services, port logistics, and freight and logistics, in Australia. | N/A |

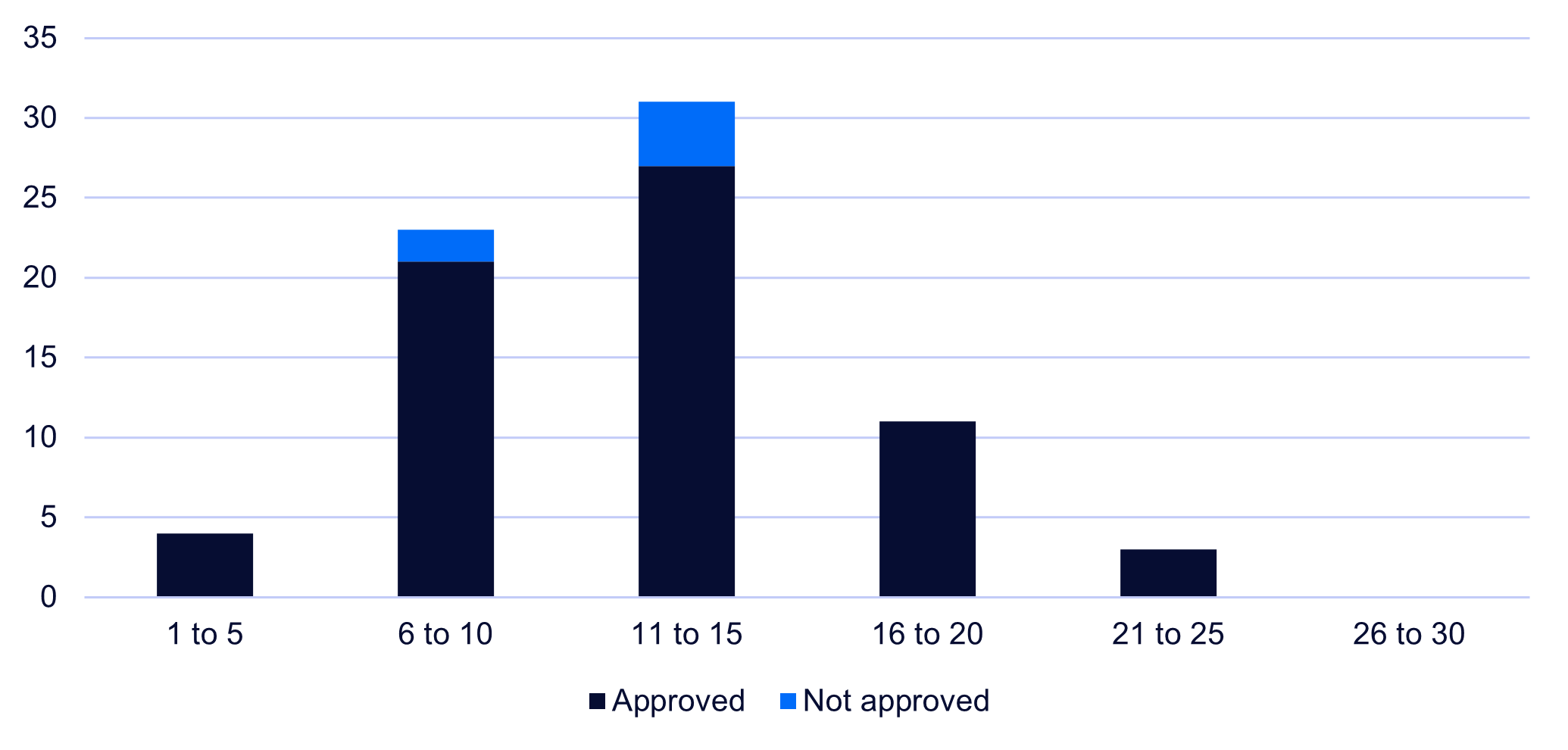

The ACCC took an average of 12 business days and a median of 12 business days to review waiver applications. This is consistent with the ACCC’s expectation that will make, in the vast majority of cases, waiver determinations within 20 business days of receiving an application. Below is a graph showing the distribution of timeframes for waiver determinations in the first quarter.

Number of business days for review of waiver determination (1 January to 31 March 2026)

Timeframes for pre-notification engagement processes

The ACCC expects the pre-notification engagement process to be capable of completion in 2 weeks for straightforward matters and at least four weeks for acquisitions raising competition concerns (ACCC merger process guidelines, December 2025, paragraph 4.8 to4.9). Based on our internal record keeping (of mergers on which we are advising), the pre-notification engagement process has taken on average 15.3 business days. However, we are aware of complex deals where pre-notification engagement has been substantially longer, and in some cases more than two months. In complex deals, the ACCC has been using the process to facilitate multiple rounds of information requests and market inquiries.

Merger reform FAQs

The table below summarises the ACCC’s updates to the merger reform FAQs during the first quarter.

Date of ACCC update

-

Fee payment instructions / Waiver v notification

Connected entities

Key changes

The ACCC provided further details on:

- fee payment;

- pre-notification and waiver processes. The ACCC confirmed that it does not recommend lodging a notification and waiver application at the same time, and that in many cases it is likely to be appropriate to lodge a notification waiver application without prior engagement with the ACCC;

- information that should be provided where there are a large number of connected entities. As a general rule, each reference in each of the forms to a ‘party to the acquisition’ is a reference to each principal party to the acquisition, the target, and each connected entity of the principal party and target. Where the parties are unsure about how to answer a particular question in respect of a specific acquisition, we suggest engaging in early discussions with the ACCC before lodging a notification or notification waiver application.

-

Discrete assets not within the aggregated turnover test

Key changes

The ACCC explained:

- its views on whether the grant of a new licence gives rise to an acquisition for the purposes of the merger control regime and confirmed that it considers acquisitions of discrete assets (being acquisitions which do not have the effect that a person will, or can acquire all or substantially all of the assets of a business) fall outside the scope of the creeping or serial acquisitions provisions in Section 2-3 of the Determination;

- further administrative details on waiver applications (including that applications should identify each of the acquirer’s and target’s site(s) in each local area where there is an actual or potential overlap) and forms and portal processes.

-

Discrete assets not within the aggregated turnover test

Key changes

The ACCC added further detail related to process and updated its response regarding how the serial acquisitions threshold could apply to acquisitions of discrete assets. Specifically, the ACCC considers that following the amendments to Section 1-10 of the Determination registered on 18 December 2025, acquisitions of ‘discrete’ assets (that is, acquisitions that do not have the effect that a person can acquire ‘all, or substantially all, of the assets of a business’) will not generally meet the creeping or serial acquisition provisions in Section 2-3.

-

Filing process

Key changes

The ACCC clarified the information required for the notification/waiver forms, and some process points. In particular:

- If a party to the acquisition has an ABN this must be provided. If a party does not have an ABN, an ACN or another similar unique identifier should be provided instead.

- Notifications and notification waiver applications must accurately identify the applicant and all parties to the acquisition to which the notification or application relates. It is the responsibility of the notifying party or applicant to ensure that the notification or notification waiver application accurately identifies all parties to the acquisition, including where those parties are subsidiaries.

- When providing market shares, notifying parties and applicants must identify the sources used to calculate market shares and provide underlying data and supporting documents where available to confirm the calculation. The ACCC recognises that precise market share information is not always possible to obtain. Where estimates are provided, parties must identify the metrics, sources, methodology and assumptions used. If value and volume are not the most common metrics for market shares in the relevant markets, provide market shares based on alternative metrics and explain why. Parties to an acquisition should have close regard to how their own internal reports or documents report on market shares or relative competitive positions. It is important that the market share estimates provided represent the parties’ best estimate, and are not biased towards understating market shares. The ACCC does not consider it is appropriate, in most cases, to rely solely on industry size estimates from IBIS reports, ABS statistics or other broad statistical data sources to estimate the relevant market size (or denominator) for calculating market shares.

- Unlike notifications, the ACCC does not expect to engage in early discussions in relation to potential notification waiver applications as a matter of course. The notification waiver process is intended for straightforward acquisitions that can be assessed based on the information provided with the application and without the need for further investigation.

The ACCC appears to be applying the new regime strictly and continues to update its guidance

The ACCC’s role as administrative decision-maker marks a significant shift under the new regime. It is taking a robust approach before exercising its administrative powers, including by applying the regime strictly and conducting thorough inquiries across matters.The ACCC has also continued to issue new guidance in the first quarter of 2026 via its merger reform FAQs. While this guidance is welcome, the regime is complex and there remains uncertainty over how it applies. By way of example, the complexity and uncertainty are demonstrated by the ACCC’s change in position in relation to a question about whether acquisitions of discrete assets are relevant for the creeping or serial acquisitions threshold—the ACCC’s initial answer was an emphatic ‘no’, but it then reversed its position in a later iteration of the FAQs document. We expect the ACCC guidance will continue to evolve as the new regime further beds down.

G+T stayed at the forefront of merger notifications by advising on more than 1 in 4 merger notifications under the new regime.

Get in touch to discuss your next transaction, or explore MerTL, our tech-enabled tool designed to quickly assess whether a deal triggers ACCC notification and streamline early-stage planning