Since the introduction of the demerger rules in Division 125 of the Tax Act in 2002, Gilbert + Tobin has advised on numerous demergers, including some landmark transactions, such as the first three-way demerger and scrip-for-scrip acquisition involving Foodland, Metcash and Woolworths. Over that time, we have seen a narrowing by the Commissioner of Taxation (ATO) of the scope of the demerger provisions.

Most recently, in June 2018, the ATO advised our client, AMA Group Limited (AMA Group), that demerger relief was not available in respect of the proposed transaction. The AMA Group withdrew its private ruling application, and the ATO will therefore not issue a ruling in respect of the transaction. Without a ruling, we must surmise the reasons for the ATO’s views, but we note the ATO is expected to issue further guidance relevant to the demerger rules later this year and next year in this regard.

Key takeaways on the ATO's ruling on demergers

Demergers typically occur in one of two scenarios, in our experience:

- A conglomerate separates itself into two distinct businesses (an example is the current proposal by the Wesfarmers group to demerge Coles); and

- The same separation occurs but in the context of a third party wishing to acquire one of those businesses (as was the case in the AMA Group demerger).

The key point going forward is that, if the ATO holds the position that we think it has taken with the AMA Group, the ATO has shut down the ability to obtain a tax-free demerger in scenario 2. However, tax-free demergers remain available in scenario 1.

What is a demerger?

A demerger broadly involves a restructuring of a corporate group by splitting it into two corporate groups (let us refer to them as the demerger group, the group undertaking the demerger, and the demerged group, the group that is demerged). Both the demerger group and the demerged group will be owned directly and in the same proportions by the existing shareholders (Shareholders) of the pre-demerger group.

If the demerger rules apply:

- The demerger group is not subject to capital gains tax (CGT) on the disposal of the demerged group; and

- Shareholders are not subject to tax on receiving shares in the demerged group (this may otherwise be subject to tax as a capital return subject to CGT or a dividend subject to ordinary income tax).

In order for demerger relief to apply, a “demerger” must happen, which requires:

- A “restructuring” of the demerger group;

- Under the restructuring, the demerger group must dispose of at least 80% of the shares in the demerged group to the Shareholders;

- Importantly for this discussion, the Shareholders must acquire shares in the demerged group, and nothing else (nothing else requirement); and

- The Shareholders must acquire the same proportion of demerged shares and proportionate market value in the demerged group as it had in the demerger group.

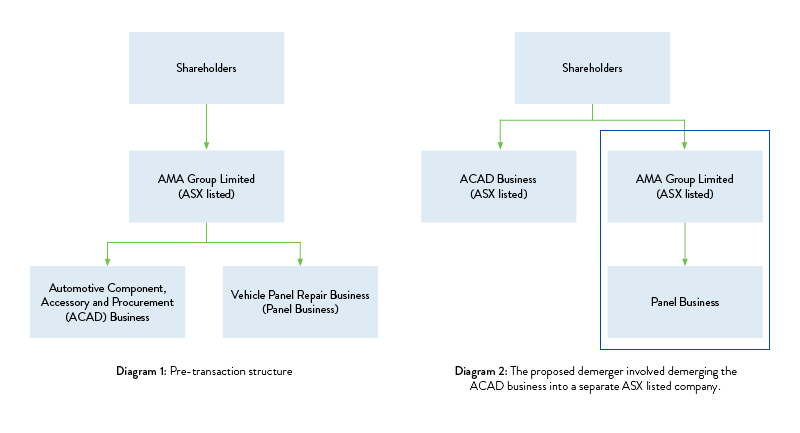

The AMA Group transaction

The AMA Group proposed to demerge its Automotive Component, Accessory and Procurement Business (ACAD Business) while retaining its Vehicle Panel Repair Business (Panel Business), as shown in the following diagrams.

The Blackstone Group (Blackstone) proposed to acquire the Panel Business (that is, the demerger group) following the demerger. Importantly, to satisfy the nothing else requirement, the demerger was not conditional on the proposed acquisition of the demerger group by Blackstone.

The ATO’s changing approach

The nothing else requirement requires Shareholders to acquire shares and nothing else (such as cash or something of value).

The ATO used to accept the situation where the demerged group was the subject of a takeover after the demerger, provided the demerger was not conditional on a subsequent acquisition occurring, as was the case in the demerger involving Foodland, Metcash and Woolworths.

The ATO eventually changed its position and accepted the situation where it was the demerger group that was the subject of the takeover, such as where Buru Energy Ltd was demerged from ARC Energy Ltd. ARC Energy Ltd was later acquired by AWE Ltd, and both the demerger and acquisition formed part of the scheme. The ATO also granted demerger relief where the demerger of Talon Petroleum Limited from Texon Petroleum Limited was a condition precedent to Texon’s subsequent acquisition by Sundance Energy Australia Limited.

However, the ATO’s most recent position is reflected in its views in the AMA Group transaction as well as in recent class rulings, such as CR 2018/31 relating to the Westfield Group acquisition by Unibail-Rodamco SE. Notwithstanding the absence of any conditionality between the demerger and the acquisition, and notwithstanding that it was the demerger group that was the subject of the acquisition, it appears to us the ATO has most likely branded the demerger and acquisition as a single restructure such that the cash or shares to be received from the takeover would have breached the nothing else requirement.

It is clear that the availability of demerger relief where a demerger is followed by a subsequent sale is now more difficult, if not impossible. Future demergers, motivated by a possible sale, need to be carefully considered in light of the moving goalposts.

Recent developments as at November 2018

Perhaps in an effort to communicate its views and provide more certainty to taxpayers, the ATO has flagged in its register of advice under development that it will provide guidance on:

- The meaning of a “restructuring” for the purposes of the demerger rules. In particular the ATO will provide guidance on how to establish the scope of a restructuring which sets the factual parameters for the application of certain conditions that must be satisfied to qualify as a demerger. The expected completion of the ATO advice is December 2018.

- Sequential planned transactions where a CGT roll-over is claimed for each transaction and the first roll-over contains a “nothing else” condition. Specifically, the ATO will provide guidance on whether the “nothing else” requirement can be satisfied if after the first transaction (for which CGT roll-over is sought), another transaction is planned under which the same entities will acquire or receive something. The expected completion of the ATO advice is May 2019.

We welcome the clarification of the ATO’s views.

Visit Smart Counsel