On 7 June 2023, the Australian Government released its Strategic Plan for Australia’s Payments System (Strategic Plan), outlining the Government’s policy objectives and priorities for reform. The Strategic Plan follows the Treasury’s recent consultation on proposed priorities and reform objectives, with an agenda focused on:

promoting a safe and resilient system;

updating the payments regulatory framework;

modernising payments infrastructure;

uplifting competition, productivity and innovation across the economy; and

keeping Australia as the leader in the global payments landscape.

The Government notes its principles to guide the future direction of Australia’s payments framework are ‘trustworthiness ’, ‘ accessibility innovation ’ and ‘efficiency ’. This is underpinned by the increasing digitisation of Australia’s payments systems, driven by consumer preferences for frictionless transactions and evolving technology. The Strategic Plan comes after over four separate payments system reviews in recent years and the previous Government’s commitment to implementing the majority of those recommendations.

Key Priorities and Initiatives: Unpacking the Government's Strategic Plan

As noted, the Strategic Plan sets out five categories of the Government’s key priorities and supporting initiatives.

| Key priority | Supporting initiatives | Next steps |

| Reducing the prevalence of scams and fraud | In 2022, Australians lost a record $3.1 billion to scams. Government, law enforcement, consumer advocacy groups and the private sector look to improve efforts to fight scams. The Government proposes to bring together private and public resources to enable better collaboration, information sharing and coordinated disruption of scams. The Government will also consider options to bolster consumer protections. | The Government is establishing the National Anti-Scam Centre, and will consult on options for developing new industry codes across sectors, including for banks, telecommunications, and digital platforms in 2023. The Government will bolster consumer protections through the new payments licensing framework. |

| Strengthening defences against cyber attacks | Recent cyber incidents have shown that the damage can be detrimental, impacting many individuals and resulting in theft of personal information. The Government plays an important role in managing cyber risk through design of legislation and regulation and coordinating with industry. The Government recently announced the establishment of a National Coordinator for Cyber Security, as well as the development of the 2023-2030 Cyber Security Strategy. AusPayNet has commenced planning for an industry-wide program to migrate the Australian card payments system to the Advanced Encryption Standard, together with improvements to cryptographic key management practices. AusPayNet plans to develop a program of work for this migration over the next 18 months, with a view to initiating an industry migration program in 2025. | The Government is releasing its Cyber Security Strategy 2023-2030 in 2023. Industry will begin migration to the Advanced Encryption Standard in 2025. |

| Supervising systematically important payment systems | The movement towards more electronic payments means payment systems are susceptible to system outages, malfunctions and flow-on impacts resulting from external shocks to other core infrastructure. Outages in payment systems can cause significant inconvenience to customers. This has increased in recent years. In response, the Reserve Bank of Australia (RBA) and Payments System Board are engaging with industry and expanding system resilience supervision to include payment systems where an outage could cause significant economic disruption and damage confidence in the financial system. | The RBA is extending its supervision from systemically important systems to also include prominent payment systems (ie, NPP, Visa, Mastercard and eftpos). The RBA will consult industry on the development and implementation of an updated framework for monitoring safety and resilience of prominent payment systems. |

Key priority

Supporting initiatives

Next steps

Reducing the prevalence of scams and fraud

In 2022, Australians lost a record $3.1 billion to scams. Government, law enforcement, consumer advocacy groups and the private sector look to improve efforts to fight scams.

The Government proposes to bring together private and public resources to enable better collaboration, information sharing and coordinated disruption of scams.

The Government will also consider options to bolster consumer protections.

The Government is establishing the National Anti-Scam Centre, and will consult on options for developing new industry codes across sectors, including for banks, telecommunications, and digital platforms in 2023.

The Government will bolster consumer protections through the new payments licensing framework.

Strengthening defences against cyber attacks

Recent cyber incidents have shown that the damage can be detrimental, impacting many individuals and resulting in theft of personal information.

The Government plays an important role in managing cyber risk through design of legislation and regulation and coordinating with industry.

The Government recently announced the establishment of a National Coordinator for Cyber Security, as well as the development of the 2023-2030 Cyber Security Strategy.

AusPayNet has commenced planning for an industry-wide program to migrate the Australian card payments system to the Advanced Encryption Standard, together with improvements to cryptographic key management practices. AusPayNet plans to develop a program of work for this migration over the next 18 months, with a view to initiating an industry migration program in 2025.

The Government is releasing its Cyber Security Strategy 2023-2030 in 2023.

Industry will begin migration to the Advanced Encryption Standard in 2025.

Supervising systematically important payment systems

The movement towards more electronic payments means payment systems are susceptible to system outages, malfunctions and flow-on impacts resulting from external shocks to other core infrastructure.

Outages in payment systems can cause significant inconvenience to customers. This has increased in recent years. In response, the Reserve Bank of Australia (RBA ) and Payments System Board are engaging with industry and expanding system resilience supervision to include payment systems where an outage could cause significant economic disruption and damage confidence in the financial system.

The RBA is extending its supervision from systemically important systems to also include prominent payment systems (ie, NPP, Visa, Mastercard and eftpos).

The RBA will consult industry on the development and implementation of an updated framework for monitoring safety and resilience of prominent payment systems.

| Key priority | Supporting initiatives | Next steps |

| Implementing changes to the Payment Systems (Regulation) Act 1998 (Cth) | New payment services and technologies are testing the limits of the current regulatory framework for the payments system. Several recent reviews have identified regulatory gaps (see our update here). In response, the Government will update the Payment Systems (Regulation) Act 1998 (Cth) (PSRA) and introduce a new payments licensing framework. These changes will involve: (a) expanding the regulatory perimeter of the PSRA by updating existing definitions of ‘payment system’ and ‘participant’ to capture all entities that play a role in facilitating or enabling payments, and (b) introducing new Ministerial powers that can be exercised in the ‘national interest’. | The Government is consulting on updates to the PSRA and the introduction of a new Ministerial designation power to inform the development of exposure draft legislation for these changes. The Government will introduce legislation to implement the PSRA changes and introduce a new Ministerial designation power by end 2023, subject to consultation outcomes. |

| Establishing a new payments licensing framework and promoting competition by facilitating transparent access to payment systems | As above, there are significant regulatory gaps in Australia’s licensing framework. The Government will consult on a new licensing framework for payment service providers. The Government intends to introduce legislation for the new payments licensing regime in 2024, including implementing the recommendations made by the Council of Financial Regulators on the regulation of stored-value facilities. Subject to legislation, detailed elements of the payments licensing reforms will be subject to further consultation. They include supporting regulations for the ePayments Code, common access requirements, and mandatory industry standards | The Government is consulting on the new licensing framework for payment service providers. This will be followed by a second round of consultation in late 2023 on the obligations under the new licensing framework. The Government will introduce legislation for the new payments licensing regime in 2024, subject to consultation outcomes. |

| Enabling greater collaboration between payment system regulators | Payment service providers have commented on the lack of transparency in the current governance and regulatory structure. Treasury established the Inter-Agency Payments Forum (IAPF) in July 2022 to improve communication and regulatory approaches regarding payments system issues. This includes participants from the RBA, APRA, ASIC, the ACCC and AUSTRAC. The IAPF is not intended to be a decision-making body. Rather, it is a forum for relevant regulators to collaborate on payments-related issues on a regular basis and avoid conflict of regulation. | The IAPF will aim to strengthen collaboration and communication between payment system regulators. |

| Reducing small business transaction costs | Greater use of debit cards is putting upward pressure on businesses’ payment costs. The growth in contactless payments has resulted in most debit card transactions being automatically routed to the international schemes instead of domestic eftpos. This is (on average) 20 basis points more expensive. The Government previously implemented least-cost routing (LCR), which allows businesses to select the lowest cost payment network. This is available for 85% of in-store merchants. Implementation for online and mobile wallet transactions is much lower. The RBA has been prioritising LCR implementation and has set its expectations for 2023. The Government supports this and will monitor LCR availability and adoption across payment methods. | The RBA will continue to publish institution level data on LCR availability and take-up. The Government is consulting on updates to the PSRA and will introduce legislation to expand the payments regulatory perimeter and bring into scope payment systems and participants such as mobile wallet providers by the end of 2023, subject to consultation outcomes. The majority of payment service providers to enable LCR for online payments by mid 2023, in line with the RBA’s expectations. Mobile wallet providers, and other industry participants as necessary, to enable LCR on mobile wallet transactions by the end of 2024, in line with the RBA’s expectations. The Government will continue to monitor payment costs for small businesses and will directly intervene if necessary. |

Key priority

Supporting initiatives

Next steps

Implementing changes to the Payment Systems (Regulation) Act 1998 (Cth)

New payment services and technologies are testing the limits of the current regulatory framework for the payments system. Several recent reviews have identified regulatory gaps (see our update here).

In response, the Government will update the Payment Systems (Regulation) Act 1998 (Cth) (PSRA ) and introduce a new payments licensing framework.

These changes will involve: (a) expanding the regulatory perimeter of the PSRA by updating existing definitions of ‘payment system’ and ‘participant’ to capture all entities that play a role in facilitating or enabling payments, and (b) introducing new Ministerial powers that can be exercised in the ‘national interest’.

The Government is consulting on updates to the PSRA and the introduction of a new Ministerial designation power to inform the development of exposure draft legislation for these changes.

The Government will introduce legislation to implement the PSRA changes and introduce a new Ministerial designation power by end 2023, subject to consultation outcomes.

Establishing a new payments licensing framework and promoting competition by facilitating transparent access to payment systems

As above, there are significant regulatory gaps in Australia’s licensing framework. The Government will consult on a new licensing framework for payment service providers.

The Government intends to introduce legislation for the new payments licensing regime in 2024, including implementing the recommendations made by the Council of Financial Regulators on the regulation of stored-value facilities. Subject to legislation, detailed elements of the payments licensing reforms will be subject to further consultation. They include supporting regulations for the ePayments Code, common access requirements, and mandatory industry standards

The Government is consulting on the new licensing framework for payment service providers. This will be followed by a second round of consultation in late 2023 on the obligations under the new licensing framework.

The Government will introduce legislation for the new payments licensing regime in 2024, subject to consultation outcomes.

Enabling greater collaboration between payment system regulators

Payment service providers have commented on the lack of transparency in the current governance and regulatory structure.

Treasury established the Inter-Agency Payments Forum (IAPF ) in July 2022 to improve communication and regulatory approaches regarding payments system issues. This includes participants from the RBA, APRA, ASIC, the ACCC and AUSTRAC.

The IAPF is not intended to be a decision-making body. Rather, it is a forum for relevant regulators to collaborate on payments-related issues on a regular basis and avoid conflict of regulation.

The IAPF will aim to strengthen collaboration and communication between payment system regulators.

Reducing small business transaction costs

Greater use of debit cards is putting upward pressure on businesses’ payment costs. The growth in contactless payments has resulted in most debit card transactions being automatically routed to the international schemes instead of domestic eftpos. This is (on average) 20 basis points more expensive.

The Government previously implemented least-cost routing (LCR ), which allows businesses to select the lowest cost payment network. This is available for 85% of in-store merchants. Implementation for online and mobile wallet transactions is much lower.

The RBA has been prioritising LCR implementation and has set its expectations for 2023. The Government supports this and will monitor LCR availability and adoption across payment methods.

The RBA will continue to publish institution level data on LCR availability and take-up.

The Government is consulting on updates to the PSRA and will introduce legislation to expand the payments regulatory perimeter and bring into scope payment systems and participants such as mobile wallet providers by the end of 2023, subject to consultation outcomes.

The majority of payment service providers to enable LCR for online payments by mid 2023, in line with the RBA’s expectations.

Mobile wallet providers, and other industry participants as necessary, to enable LCR on mobile wallet transactions by the end of 2024, in line with the RBA’s expectations.

The Government will continue to monitor payment costs for small businesses and will directly intervene if necessary.

| Key priority | Supporting initiatives | Next steps |

| Phasing out cheques | There has been a rapid decline in the use of cheques in the past 10 years, which now comprise only 0.2 per cent of non-cash payments in Australia. As cheque use declines, the per-transaction cost of supporting the cheque system will continue to increase. The Government will focus on removing legislative and other barriers that entrench payment by cheques as well as phasing out government cheque usage by the end of 2028, with the eventual wind-down of the cheques system in Australia by no later than 2030. | In 2023, Treasury will commence engagement with relevant Commonwealth, state and territory government agencies, on transitioning away from the use of cheques. The Government will remove barriers that entrench payment for goods and services by cheques. In 2023, Treasury will commence exploring changes to the Commonwealth legislation that entrenches the use and acceptance of cheques. The Government will release a consultation paper on the future of cheque use in Australia, and the support required to retire the cheques system. |

| Upgrading systems | One of the legacy payment systems operating in Australia is the Bulk Electronic Clearing System (BECS). BECS is a long-running electronic funds transfer system that facilitates the processing of direct entry payments. Since the introduction of the New Payments Platform (NPP) there have been key features launched that provide significant advantages over BECS (faster payments, data rich payments, safer payments). AusPayNet is currently consulting industry and key users on the future of BECS, including feasible timeframes or preconditions for transitioning different transaction types onto alternative payment systems. Transitioning direct debits to the NPP is a major milestone in modernising consumer facing payments. | The Government is supporting a phased transition away from BECS. Industry to settle on a transition plan away from BECS by the end of 2023. NPP Australia and NPP Participants to consider how the process of transitioning bulk payments away from BECS could be made as efficient as possible for users in minimising the cost of internal systems changes. Treasury will engage with NPP Australia and NPP Participants in the lead-up to the next strategic plan to take stock of progress. Treasury will commence engagement with relevant Commonwealth, state and territory government agencies and other key users of BECS bulk payments on their needs and readiness to transition away from BECS. Industry will by mid-2023 make PayTo available on most NPP enabled accounts, in line with October 2022 NPP Roadmap. Financial institutions will report on progress to the RBA on their work connecting all relevant accounts to the NPP. |

| Maintaining access to cash | Cash is an important payment method for certain groups in Australia and plays a vital role in their inclusion in the wider economy. However, the use of cash as a method of payment has declined substantially in the last decade and this trend accelerated during the COVID-19 pandemic. The declining transactional use of cash has led to a per unit increase in costs in distributing cash across the country. Australia’s two largest Cash-in-Transit (CIT) service providers, Armaguard and Prosegur, have responded to these financial pressures in recent years by downsizing or closing some facilities and reducing the frequency of CIT services. The Government will closely monitor developments regarding access to cash for Australians, in close consultation with relevant regulators. | The Government will support Australians having continued access to cash. The Senate Standing Committee on Rural and Regional Affairs and Transport will by 1 December 2023 release its report on Bank Closures in Regional Australia. In 2023, Treasury will commence engagement with relevant Commonwealth government agencies and industry on options for maintaining adequate access to cash for as long as Australians want to use cash. |

Key priority

Supporting initiatives

Next steps

Phasing out cheques

There has been a rapid decline in the use of cheques in the past 10 years, which now comprise only 0.2 per cent of non-cash payments in Australia. As cheque use declines, the per-transaction cost of supporting the cheque system will continue to increase.

The Government will focus on removing legislative and other barriers that entrench payment by cheques as well as phasing out government cheque usage by the end of 2028, with the eventual wind-down of the cheques system in Australia by no later than 2030.

In 2023, Treasury will commence engagement with relevant Commonwealth, state and territory government agencies, on transitioning away from the use of cheques.

The Government will remove barriers that entrench payment for goods and services by cheques.

In 2023, Treasury will commence exploring changes to the Commonwealth legislation that entrenches the use and acceptance of cheques.

The Government will release a consultation paper on the future of cheque use in Australia, and the support required to retire the cheques system.

Upgrading systems

One of the legacy payment systems operating in Australia is the Bulk Electronic Clearing System (BECS ). BECS is a long-running electronic funds transfer system that facilitates the processing of direct entry payments.

Since the introduction of the New Payments Platform (NPP ) there have been key features launched that provide significant advantages over BECS (faster payments, data rich payments, safer payments).

AusPayNet is currently consulting industry and key users on the future of BECS, including feasible timeframes or preconditions for transitioning different transaction types onto alternative payment systems. Transitioning direct debits to the NPP is a major milestone in modernising consumer facing payments.

The Government is supporting a phased transition away from BECS.

Industry to settle on a transition plan away from BECS by the end of 2023.

NPP Australia and NPP Participants to consider how the process of transitioning bulk payments away from BECS could be made as efficient as possible for users in minimising the cost of internal systems changes. Treasury will engage with NPP Australia and NPP Participants in the lead-up to the next strategic plan to take stock of progress.

Treasury will commence engagement with relevant Commonwealth, state and territory government agencies and other key users of BECS bulk payments on their needs and readiness to transition away from BECS.

Industry will by mid-2023 make PayTo available on most NPP enabled accounts, in line with October 2022 NPP Roadmap.

Financial institutions will report on progress to the RBA on their work connecting all relevant accounts to the NPP.

Maintaining access to cash

Cash is an important payment method for certain groups in Australia and plays a vital role in their inclusion in the wider economy. However, the use of cash as a method of payment has declined substantially in the last decade and this trend accelerated during the COVID-19 pandemic.

The declining transactional use of cash has led to a per unit increase in costs in distributing cash across the country. Australia’s two largest Cash-in-Transit (CIT ) service providers, Armaguard and Prosegur, have responded to these financial pressures in recent years by downsizing or closing some facilities and reducing the frequency of CIT services.

The Government will closely monitor developments regarding access to cash for Australians, in close consultation with relevant regulators.

The Government will support Australians having continued access to cash.

The Senate Standing Committee on Rural and Regional Affairs and Transport will by 1 December 2023 release its report on Bank Closures in Regional Australia.

In 2023, Treasury will commence engagement with relevant Commonwealth government agencies and industry on options for maintaining adequate access to cash for as long as Australians want to use cash.

| Key priority | Supporting initiatives | Next steps |

| Aligning payments system objectives and the CDR framework | The Consumer Data Right (CDR) enables consumers to safely access certain data about them held by businesses and share this data with accredited third parties. While both the CDR and payment systems continue to evolve, the Government is committed to aligning developments under the CDR framework with its broader objectives for the payments system. | The Government will continue working with stakeholders on the potential interaction between the CDR framework and the payments system. Under the CDR action initiation framework, the Government will carry out an assessment and publicly consult before bringing any action types, such as payments, into the CDR. |

| Supporting the broader use of Digital ID | Digital ID will be a voluntary, secure and trusted way to verify a person’s identity online, while minimising collection and retention of personal information. Digital ID can currently be used to access more than 125 government services, as well as private sector solutions. The Government is prioritising reform and enabling legislation to modernise Australia’s ID system and ensure a nationally coordinated approach. | The Government will continue to design the policy and legislative foundations to transition to an economy wide Digital ID ecosystem with an independent regulator. |

| Uplifting digital and technological skills | The Government is working to uplift digital and technological skills, to ensure Australians take full advantage of the digital transformation of the economy. The Government is committed to working with industry and others to deliver 1.2 million tech-related jobs by 2030. | The Government is identifying opportunities to build the digital skills needed for the Australian economy. The Government will consider a report by the Digital and Tech Skills Working Group, established at the Jobs and Skills Summit, on an ‘earn-while-you-learn’ model of training (akin to a ‘digital apprenticeship’). The Working Group is expected to provide the report to the Government in June 2023. |

| Building public trust and confidence and supporting adoption of AI | The safe and responsible deployment and adoption of AI presents significant opportunities for Australia to improve economic and social outcomes. The Government is taking steps to build the public trust and confidence in AI and support its adoption. | On 1 June 2023, the Government released a discussion paper entitled ‘Safe and responsible AI in Australia’. The Government will consult on how it can support the safe and responsible use of AI, and ultimately increase community trust and confidence. |

Key priority

Supporting initiatives

Next steps

Aligning payments system objectives and the CDR framework

The Consumer Data Right (CDR ) enables consumers to safely access certain data about them held by businesses and share this data with accredited third parties.

While both the CDR and payment systems continue to evolve, the Government is committed to aligning developments under the CDR framework with its broader objectives for the payments system.

The Government will continue working with stakeholders on the potential interaction between the CDR framework and the payments system.

Under the CDR action initiation framework, the Government will carry out an assessment and publicly consult before bringing any action types, such as payments, into the CDR.

Supporting the broader use of Digital ID

Digital ID will be a voluntary, secure and trusted way to verify a person’s identity online, while minimising collection and retention of personal information.

Digital ID can currently be used to access more than 125 government services, as well as private sector solutions.

The Government is prioritising reform and enabling legislation to modernise Australia’s ID system and ensure a nationally coordinated approach.

The Government will continue to design the policy and legislative foundations to transition to an economy wide Digital ID ecosystem with an independent regulator.

Uplifting digital and technological skills

The Government is working to uplift digital and technological skills, to ensure Australians take full advantage of the digital transformation of the economy. The Government is committed to working with industry and others to deliver 1.2 million tech-related jobs by 2030.

The Government is identifying opportunities to build the digital skills needed for the Australian economy.

The Government will consider a report by the Digital and Tech Skills Working Group, established at the Jobs and Skills Summit, on an ‘earn-while-you-learn’ model of training (akin to a ‘digital apprenticeship’). The Working Group is expected to provide the report to the Government in June 2023.

Building public trust and confidence and supporting adoption of AI

The safe and responsible deployment and adoption of AI presents significant opportunities for Australia to improve economic and social outcomes. The Government is taking steps to build the public trust and confidence in AI and support its adoption.

On 1 June 2023, the Government released a discussion paper entitled ‘Safe and responsible AI in Australia’. The Government will consult on how it can support the safe and responsible use of AI, and ultimately increase community trust and confidence.

| Key priority | Supporting initiatives | Next steps |

| Creating a regulatory environment that attracts and enables innovation | The Government recognises its role in encouraging greater cooperation in payments innovation. An industry stakeholder roundtable will be undertaken to provide an opportunity for industry to highlight areas of priority where Government can assist in facilitating industry coordination, within the limitations of competition laws. | The Government will host an industry stakeholder roundtable for the payments system. |

| Facilitating cross-border payments | Cross-border payments lag domestic payments in meeting expectations for services to be cheap, fast, accessible and transparent. G20 countries, including Australia, have endorsed a roadmap for making cross-border payments cheaper, faster, more transparent and more accessible. The Government supports the joint work of regulators and industry towards achieving the 2027 G20 targets. | NPP participants will by 1 December 2023 join the NPP International Payments Business Service to enhance the speed and efficiency of incoming cross-border payments, in line with the October 2022 NPP Roadmap. NPP Identified Institutions will by 30 April 2024 provide international payment service functionality via the NPP to enhance the speed of inbound cross-border payments, in line with the October 2022 NPP Roadmap. The RBA and industry will in 2023 explore issues associated with directly linking fast payment systems with other jurisdictions. AusPayNet, the RBA and industry will by end of 2025 fully migrate the HVCS to the ISO20022 standard. Treasury will monitor ACCC guidance on ‘Transport pricing of foreign currency conversion services’ to deliver full fee transparency, including FX margins. |

| Exploring the policy rationale for a CBDC in Australia | A central bank digital currency (CBDC) is a new digital form of money issued by a central bank and denominated in the national unit of account. As part of a broader research program into the future of public and private digital money in Australia, Treasury and the RBA with the Digital Finance Cooperative Research Centre (DFCRC) are working together to explore the policy case for an Australian CBDC. Treasury and the RBA are continuing their research on how an Australian CBDC could operate and assessing what impacts it might have on the economy and financial system. | The RBA and DFCRC will publish a report on the outcomes of the CBDC pilot in mid-2023. Treasury and the RBA will release a paper in mid-2024 that takes stock of the work to date by the Treasury and the RBA on CBDC in Australia, and outlines the forward workplan for Treasury and the RBA on CBDC in the broader context of the future of digital money in Australia. |

Key priority

Supporting initiatives

Next steps

Creating a regulatory environment that attracts and enables innovation

The Government recognises its role in encouraging greater cooperation in payments innovation. An industry stakeholder roundtable will be undertaken to provide an opportunity for industry to highlight areas of priority where Government can assist in facilitating industry coordination, within the limitations of competition laws.

The Government will host an industry stakeholder roundtable for the payments system.

Facilitating cross-border payments

Cross-border payments lag domestic payments in meeting expectations for services to be cheap, fast, accessible and transparent. G20 countries, including Australia, have endorsed a roadmap for making cross-border payments cheaper, faster, more transparent and more accessible.

The Government supports the joint work of regulators and industry towards achieving the 2027 G20 targets.

NPP participants will by 1 December 2023 join the NPP International Payments Business Service to enhance the speed and efficiency of incoming cross-border payments, in line with the October 2022 NPP Roadmap.

NPP Identified Institutions will by 30 April 2024 provide international payment service functionality via the NPP to enhance the speed of inbound cross-border payments, in line with the October 2022 NPP Roadmap.

The RBA and industry will in 2023 explore issues associated with directly linking fast payment systems with other jurisdictions.

AusPayNet, the RBA and industry will by end of 2025 fully migrate the HVCS to the ISO20022 standard.

Treasury will monitor ACCC guidance on ‘Transport pricing of foreign currency conversion services’ to deliver full fee transparency, including FX margins.

Exploring the policy rationale for a CBDC in Australia

A central bank digital currency (CBDC ) is a new digital form of money issued by a central bank and denominated in the national unit of account. As part of a broader research program into the future of public and private digital money in Australia, Treasury and the RBA with the Digital Finance Cooperative Research Centre (DFCRC ) are working together to explore the policy case for an Australian CBDC.

Treasury and the RBA are continuing their research on how an Australian CBDC could operate and assessing what impacts it might have on the economy and financial system.

The RBA and DFCRC will publish a report on the outcomes of the CBDC pilot in mid-2023.

Treasury and the RBA will release a paper in mid-2024 that takes stock of the work to date by the Treasury and the RBA on CBDC in Australia, and outlines the forward workplan for Treasury and the RBA on CBDC in the broader context of the future of digital money in Australia.

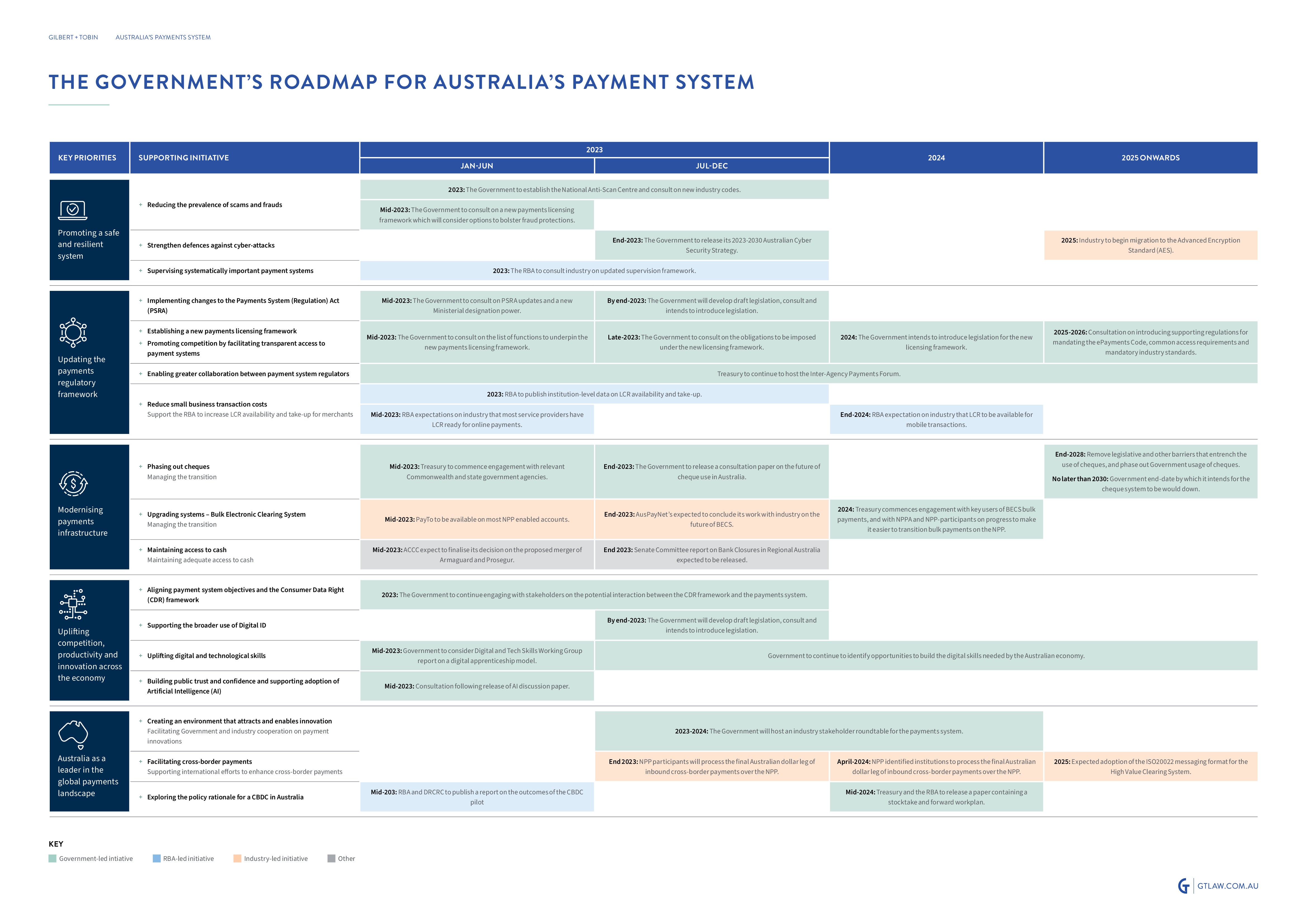

Roadmap for Australia’s Payments system

As part of the Strategic Plan, the Government provided guidance regarding the rollout of its proposed supporting initiatives.

Considering options: Strategic Plan's Long-Term Impact on Payment and Payment Technology Providers

Many of the proposals in the Strategic Plan are not new, but reaffirm the Government’s previous commitments to recommendations in various payments reviews over the years. However, some proposals have the potential to radically impact the regulatory touchpoints for payment and payment technology providers in the longer term. While these areas are subject to further consultation, payments providers should consider the potential impact for their business and whether participation in Treasury consultations would assist in shaping any future reform.